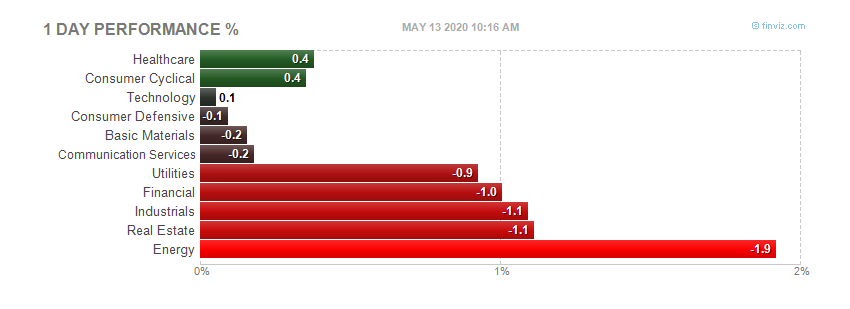

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Breaking news just now from CNBC said Roubini was misquoted.

I got a screen shot of their website before the link doesn't work.

Here is the original link

The Fast Money crew is spinning this so bad it's comical. They have been toting this call since they reported it around the time the market launched. Even had a graphic after the close calling it the "Roubini Rally."

From Roubini's website:

Nouriel Roubini | Jul 16, 2009

“It has been widely reported today that I have stated that the recession will be over “this year” and that I have “improved” my economic outlook. Despite those reports - however – my views expressed today are no different than the views I have expressed previously. If anything my views were taken out of context.

“I have said on numerous occasions that the recession would last roughly 24 months. Therefore, we are 19months into that recession. If, as I predicted, the recession is over by year end, it will have lasted 24 months with a recovery only beginning in 2010. Simply put I am not forecasting economic growth before year’s end.

“Indeed, last year I argued that this will be a long and deep and protracted U-shaped recession that would last 24 months. Meanwhile, the consensus argued that this would be a short and shallow V-shaped 8 months long recession (like those in 1990-91 and 2001). That debate is over today as we are in the 19th month of a severe recession; so the V is out the window and we are in a deep U-shaped recession. If that recession were to be over by year end – as I have consistently predicted – it would have lasted 24 months and thus been three times longer than the previous two and five times deeper – in terms of cumulative GDP contraction – than the previous two. So, there is nothing new in my remarks today about the recession being over at the end of this year.

“I have also consistently argued – including in my remarks today - that while the consensus predicts that the US economy will go back close to potential growth by next year, I see instead a shallow, below-par and below-trend recovery where growth will average about 1% in the next couple of years when potential is probably closer to 2.75%.

“I have also consistently argued that there is a risk of a double-dip W-shaped recession toward the end of 2010, as a tough policy dilemma will emerge next year: on one side, early exit from monetary and fiscal easing would tip the economy into a new recession as the recovery is anemic and deflationary pressures are dominant. On the other side, maintaining large budget deficits and continued monetization of such deficits would eventually increase long term interest rates (because of concerns about medium term fiscal sustainability and because of an increase in expected inflation) and thus would lead to a crowding out of private demand.

“While the recession will be over by the end of the year the recovery will be weak given the debt overhang in the household sector, the financial system and the corporate sector; and now there is also a massive re-leveraging of the public sector with unsustainable fiscal deficits and public debt accumulation.

“Also, as I fleshed out in detail in recent remarks the labor market is still very weak: I predict a peak unemployment rate of close to 11% in 2010. Such large unemployment will have negative effects on labor income and consumption growth; will postpone the bottoming out of the housing sector; will lead to larger defaults and losses on bank loans (residential and commercial mortgages, credit cards, auto loans, leveraged loans); will increase the size of the budget deficit (even before any additional stimulus is implemented); and will increase protectionist pressures.

“So, yes there is light at the end of the tunnel for the US and the global economy; but as I have consistently argued the recession will continue through the end of the year, and the recovery will be weak and at risk of a double dip, as the challenge of getting right the timing and size of the exit strategy for monetary and fiscal policy easing will be daunting.

“RGE Monitor will soon release our updated U.S. and Global Economic Outlook. A preview of the U.S. Outlook is available on our website: www.rgemonitor.com”

Breaking news just now from CNBC said Roubini was misquoted.

I got a screen shot of their website before the link doesn't work.

Here is the original link

The Fast Money crew is spinning this so bad it's comical. They have been toting this call since they reported it around the time the market launched. Even had a graphic after the close calling it the "Roubini Rally."

From Roubini's website:

Nouriel Roubini | Jul 16, 2009

“It has been widely reported today that I have stated that the recession will be over “this year” and that I have “improved” my economic outlook. Despite those reports - however – my views expressed today are no different than the views I have expressed previously. If anything my views were taken out of context.

“I have said on numerous occasions that the recession would last roughly 24 months. Therefore, we are 19months into that recession. If, as I predicted, the recession is over by year end, it will have lasted 24 months with a recovery only beginning in 2010. Simply put I am not forecasting economic growth before year’s end.

“Indeed, last year I argued that this will be a long and deep and protracted U-shaped recession that would last 24 months. Meanwhile, the consensus argued that this would be a short and shallow V-shaped 8 months long recession (like those in 1990-91 and 2001). That debate is over today as we are in the 19th month of a severe recession; so the V is out the window and we are in a deep U-shaped recession. If that recession were to be over by year end – as I have consistently predicted – it would have lasted 24 months and thus been three times longer than the previous two and five times deeper – in terms of cumulative GDP contraction – than the previous two. So, there is nothing new in my remarks today about the recession being over at the end of this year.

“I have also consistently argued – including in my remarks today - that while the consensus predicts that the US economy will go back close to potential growth by next year, I see instead a shallow, below-par and below-trend recovery where growth will average about 1% in the next couple of years when potential is probably closer to 2.75%.

“I have also consistently argued that there is a risk of a double-dip W-shaped recession toward the end of 2010, as a tough policy dilemma will emerge next year: on one side, early exit from monetary and fiscal easing would tip the economy into a new recession as the recovery is anemic and deflationary pressures are dominant. On the other side, maintaining large budget deficits and continued monetization of such deficits would eventually increase long term interest rates (because of concerns about medium term fiscal sustainability and because of an increase in expected inflation) and thus would lead to a crowding out of private demand.

“While the recession will be over by the end of the year the recovery will be weak given the debt overhang in the household sector, the financial system and the corporate sector; and now there is also a massive re-leveraging of the public sector with unsustainable fiscal deficits and public debt accumulation.

“Also, as I fleshed out in detail in recent remarks the labor market is still very weak: I predict a peak unemployment rate of close to 11% in 2010. Such large unemployment will have negative effects on labor income and consumption growth; will postpone the bottoming out of the housing sector; will lead to larger defaults and losses on bank loans (residential and commercial mortgages, credit cards, auto loans, leveraged loans); will increase the size of the budget deficit (even before any additional stimulus is implemented); and will increase protectionist pressures.

“So, yes there is light at the end of the tunnel for the US and the global economy; but as I have consistently argued the recession will continue through the end of the year, and the recovery will be weak and at risk of a double dip, as the challenge of getting right the timing and size of the exit strategy for monetary and fiscal policy easing will be daunting.

“RGE Monitor will soon release our updated U.S. and Global Economic Outlook. A preview of the U.S. Outlook is available on our website: www.rgemonitor.com”

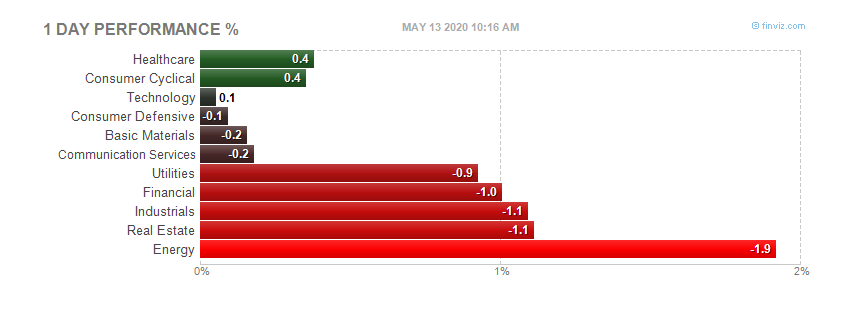

Today's heatmap:

Today's heatmap:

Notable earnings before open tomorrrow - BAC,C,GE,MAT

Ecomomic calendar - 8:30 Housing starts

Notable earnings before open tomorrrow - BAC,C,GE,MAT

Ecomomic calendar - 8:30 Housing starts

Before market opens

Before market opens

After market closes

After market closes

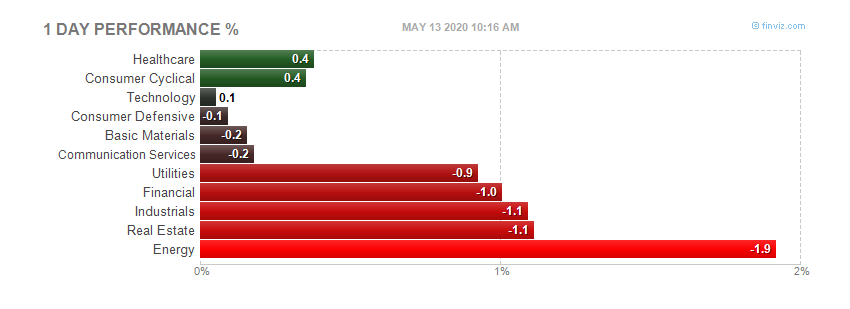

Today's heatmap:

Today's heatmap:

Notice we are not right at the right sholder of the head and shoulders pattern. We will see if the bulls can push this higher. The next level will be the head which is around the 956.23. If we would have breached the 878 - 880 level, many bears would have jumped on, the head and shoulders would have been confirmed. Now we need to see if the top is breached which might send this market on another bull run - fundamentals be damned.

Notice we are not right at the right sholder of the head and shoulders pattern. We will see if the bulls can push this higher. The next level will be the head which is around the 956.23. If we would have breached the 878 - 880 level, many bears would have jumped on, the head and shoulders would have been confirmed. Now we need to see if the top is breached which might send this market on another bull run - fundamentals be damned.

Full report here

The Empire State Manufacturing Survey indicates that conditions for New York manufacturers were flat in July. The general business conditions index increased to a level close to zero, rising 9 points, to -0.6. The new orders index rose above zero for the first time in several months, and the shipments index also climbed into positive territory. The inventories index slipped to a record-low -36.5. The prices paid index rose above zero for the first time since November, while the prices received index held below zero. Employment indexes remained well below zero. Future indexes continued to be relatively optimistic about the six-month outlook, but were somewhat less buoyant than in June. The capital spending index fell several points, but remained above zero.

In a series of supplementary questions (see Supplemental Report tab), the median respondent indicated that total sales had fallen 15 percent from the first half of 2008 to the first half of 2009, and that the number of employees had decreased 10 percent. Declines for the full year were expected to be of the same respective magnitudes. The same questions were asked in July 2008; in that survey, sales had been seen as rising 5 percent, with employment levels being little changed. When asked if they had recently modified their production plans for the second half of 2009, close to 63 percent of respondents reported that they had scaled back plans, while just 21 percent indicated that they had increased them. This result reflects a much more negative assessment than what was reported in last July’s survey. In response to an additional set of questions new to this survey, manufacturers generally reported little effect thus far from the economic stimulus package.

General Business Conditions Index Rises, Holds around Zero. The general business conditions index rose several points in July, hovering around zero for the first time since last summer, at -0.6—suggesting that conditions neither worsened nor improved over the month. Twenty-three percent observed that conditions improved, less than the 28 percent reporting so in June, while 24 percent said that conditions worsened, well below the 38 percent who saw deteriorating conditions in June. The new orders index rose above zero for the first time since September 2008, climbing from -8.2 to 5.9. The shipments index rose similarly, from -4.8 to 11.0, its highest level in a year. The unfilled orders index held steady at -12.5. The delivery time index fell 4 points, to -14.6, and the inventories index declined 11 points, to -36.5, a record low.

Input Prices Resume Increase

After several months of readings below zero, the prices paid index rose 16 points, to 10.4, the first positive value since November 2008, indicating that input prices are once again on the upswing. The prices received index remained negative, inching up 4points, to -8.3. Employment indexes remained negative and near June readings. The number of employees index was -20.8, and the average workweek index was -19.8.

Outlook Remains Favorable

The six-month outlook remained favorable in July, although future indexes were somewhat lower than last month. The future general business conditions index fell 14 points, but at 34.0 was well above the very low levels of earlier this year. The future new orders and shipments indexes also declined similarly. The future prices paid index rose 16 points, to 26.0, while the future prices received index held just below zero. Future employment indexes were positive. The capital expenditures index slipped 9 points, to 2.1, while the technology spending index held steady at 1.0.

Full report here

The Empire State Manufacturing Survey indicates that conditions for New York manufacturers were flat in July. The general business conditions index increased to a level close to zero, rising 9 points, to -0.6. The new orders index rose above zero for the first time in several months, and the shipments index also climbed into positive territory. The inventories index slipped to a record-low -36.5. The prices paid index rose above zero for the first time since November, while the prices received index held below zero. Employment indexes remained well below zero. Future indexes continued to be relatively optimistic about the six-month outlook, but were somewhat less buoyant than in June. The capital spending index fell several points, but remained above zero.

In a series of supplementary questions (see Supplemental Report tab), the median respondent indicated that total sales had fallen 15 percent from the first half of 2008 to the first half of 2009, and that the number of employees had decreased 10 percent. Declines for the full year were expected to be of the same respective magnitudes. The same questions were asked in July 2008; in that survey, sales had been seen as rising 5 percent, with employment levels being little changed. When asked if they had recently modified their production plans for the second half of 2009, close to 63 percent of respondents reported that they had scaled back plans, while just 21 percent indicated that they had increased them. This result reflects a much more negative assessment than what was reported in last July’s survey. In response to an additional set of questions new to this survey, manufacturers generally reported little effect thus far from the economic stimulus package.

General Business Conditions Index Rises, Holds around Zero. The general business conditions index rose several points in July, hovering around zero for the first time since last summer, at -0.6—suggesting that conditions neither worsened nor improved over the month. Twenty-three percent observed that conditions improved, less than the 28 percent reporting so in June, while 24 percent said that conditions worsened, well below the 38 percent who saw deteriorating conditions in June. The new orders index rose above zero for the first time since September 2008, climbing from -8.2 to 5.9. The shipments index rose similarly, from -4.8 to 11.0, its highest level in a year. The unfilled orders index held steady at -12.5. The delivery time index fell 4 points, to -14.6, and the inventories index declined 11 points, to -36.5, a record low.

Input Prices Resume Increase

After several months of readings below zero, the prices paid index rose 16 points, to 10.4, the first positive value since November 2008, indicating that input prices are once again on the upswing. The prices received index remained negative, inching up 4points, to -8.3. Employment indexes remained negative and near June readings. The number of employees index was -20.8, and the average workweek index was -19.8.

Outlook Remains Favorable

The six-month outlook remained favorable in July, although future indexes were somewhat lower than last month. The future general business conditions index fell 14 points, but at 34.0 was well above the very low levels of earlier this year. The future new orders and shipments indexes also declined similarly. The future prices paid index rose 16 points, to 26.0, while the future prices received index held just below zero. Future employment indexes were positive. The capital expenditures index slipped 9 points, to 2.1, while the technology spending index held steady at 1.0.

After market closes

After market closes

Today's heatmap:

Today's heatmap:

As their chart shows, they have been dropping quite severely, but the last two days have been really bad. But, not to worry, from Bloomberg we see this - CIT Rises on ‘Active’ Talks for U.S. Aid Before Debt Maturity - really?

From the article - July 14 (Bloomberg) -- CIT Group Inc. rose in European trading after the corporate lender said it’s in “active discussions” with regulators about a rescue before $1 billion of bonds mature next month.

ANOTHER RESCUSE/BAILOUT? Screw that, we the taxpayers have given these damn financial companies enough money. Here's an idea - LET GOLDMAN SACHS BAIL THEIR ASS OUT.

By the way, they are up over 18 percent pre-market. Investors (cough, cough) ready to jump on the government backed gravy train. Err...I mean taxpayer backed gravy train. The robbing and pillaging continues.

As their chart shows, they have been dropping quite severely, but the last two days have been really bad. But, not to worry, from Bloomberg we see this - CIT Rises on ‘Active’ Talks for U.S. Aid Before Debt Maturity - really?

From the article - July 14 (Bloomberg) -- CIT Group Inc. rose in European trading after the corporate lender said it’s in “active discussions” with regulators about a rescue before $1 billion of bonds mature next month.

ANOTHER RESCUSE/BAILOUT? Screw that, we the taxpayers have given these damn financial companies enough money. Here's an idea - LET GOLDMAN SACHS BAIL THEIR ASS OUT.

By the way, they are up over 18 percent pre-market. Investors (cough, cough) ready to jump on the government backed gravy train. Err...I mean taxpayer backed gravy train. The robbing and pillaging continues.

Before market opens

Before market opens

Today after close

Today after close

The banks win again! Can anyone tell me how these banks, half of which should be bankrupt (at least)are six and a half percent better than last week?

Today's heatmap:

The banks win again! Can anyone tell me how these banks, half of which should be bankrupt (at least)are six and a half percent better than last week?

Today's heatmap:

Lots of green there. Must be the green shoots turning into flowers.

Lots of green there. Must be the green shoots turning into flowers.

Before market opens in BOLD

Before market opens in BOLD