Friday, July 24, 2009

Gone golfing - have a good weekend - nothng to see here today it seems - 10:35AM

Have a good weekend.

Happy Trading

Pre-market - July 24 - 8:15AM

Futures pointing higher slightly this morning:

DJIA INDEX 9,018.00 27.00

S&P 500 970.90 2.00

NASDAQ 100 1,583.25 -0.75

Gold 955 2 0.16%

Oil 67.16 -0.02 -0.03%

Today's economic calendar:

Consumer Sentiment 9:55 AM ET

Today's earnings reports:

Before market opens:

Today after = EEP, MCBI

Today after = EEP, MCBI

Today after = EEP, MCBI

Today after = EEP, MCBI

Thursday, July 23, 2009

Market Wrap - 4:30PM

Another rocket upward today.

Dow 9,069.29 +188.03 (2.12%)

S&P 500 976.29 +22.22 (2.33%)

Nasdaq 1,973.60 +47.22 (2.45%)

Gold 955 +2 +0.16%

Oil 67.13 1.76 2.69%

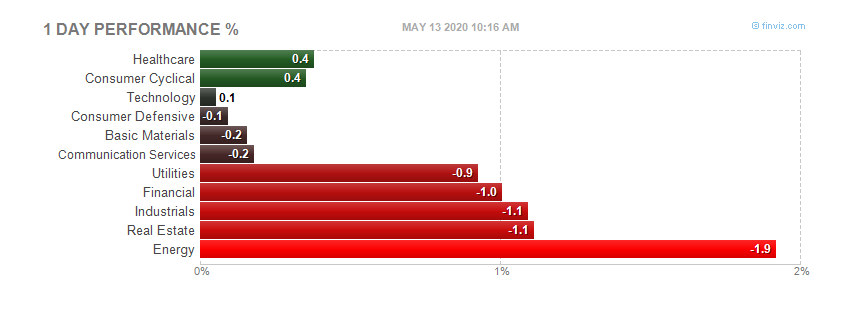

Today by sector:

Today's heatmap:

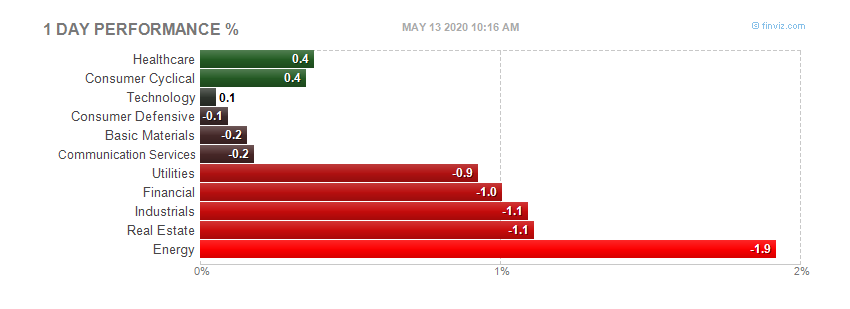

Today's heatmap:

Today's heatmap:

Jobless claims - July 23, 2009 - 8:38AM

UNEMPLOYMENT INSURANCE WEEKLY CLAIMS REPORT

SEASONALLY ADJUSTED DATA

In the week ending July 18, the advance figure for seasonally adjusted initial claims was 554,000, an increase of 30,000 from the previous week's revised figure of 524,000. The 4-week moving average was 566,000, a decrease of 19,000 from the previous week's revised average of 585,000.

The advance seasonally adjusted insured unemployment rate was 4.7 percent for the week ending July 11, unchanged from the prior week's unrevised rate of 4.7 percent.

The advance number for seasonally adjusted insured unemployment during the week ending July 11 was 6,225,000, a decrease of 88,000 from the preceding week's revised level of 6,313,000. The 4-week moving average was 6,541,500, a decrease of 132,500 from the preceding week's revised average of 6,674,000.

The fiscal year-to-date average for seasonally adjusted insured unemployment for all programs is 5.474 million.

UNADJUSTED DATA

The advance number of actual initial claims under state programs, unadjusted, totaled 580,944 in the week ending July 18, a decrease of 90,298 from the previous week. There were 411,408 initial claims in the comparable week in 2008.

The advance unadjusted insured unemployment rate was 4.7 percent during the week ending July 11, an increase of 0.1 percentage point from the prior week. The advance unadjusted number for persons claiming UI benefits in state programs totaled 6,231,108, an increase of 57,168 from the preceding week. A year earlier, the rate was 2.4 percent and the volume was 3,164,970.

Extended benefits were available in Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, the District of Columbia, Florida, Georgia, Idaho, Illinois, Indiana, Kentucky, Maine, Massachusetts, Michigan, Minnesota, Missouri, Montana, Nevada, New Jersey, New York, North Carolina, Ohio, Oregon, Pennsylvania, Puerto Rico, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, Washington, and Wisconsin during the week ending July 4.

Initial claims for UI benefits by former Federal civilian employees totaled 2,034 in the week ending July 11, an increase of 392 from the prior week. There were 2,234 initial claims by newly discharged veterans, an increase of 364 from the preceding week.

There were 18,461 former Federal civilian employees claiming UI benefits for the week ending July 4, an increase of 990 from the previous week. Newly discharged veterans claiming benefits totaled 29,098, an increase of 331 from the prior week.

States reported 2,632,361 persons claiming EUC (Emergency Unemployment Compensation) benefits for the week ending July 4, an increase of 107,019 from the prior week. EUC weekly claims include both first and second tier activity.

The highest insured unemployment rates in the week ending July 4 were in Puerto Rico (6.9 percent), Michigan (6.8), Oregon (6.8), Pennsylvania (6.4), Nevada (6.2), Wisconsin (6.1), South Carolina (5.7), New Jersey (5.6), North Carolina (5.5), and Connecticut (5.4).

The largest increases in initial claims for the week ending July 11 were in New York (+12,504), North Carolina (+10,382), Florida (+10,043), Missouri (+8,293), and Tennessee (+6,943), while the largest decreases were in Michigan (-6,648), Massachusetts (-2,910), New Jersey (-2,888), Indiana (-2,497), and California (-1,755).

Full report here

Full report here

Full report here

Full report here

Pre-market - July 23, 2009 7:45AM

Futures all over the place this morning with all the earnings coming out.

DJIA INDEX 8,851.00 18.00

S&P 500 951.50 2.10 949.60

NASDAQ 100 1,560.50 4.00

Gold 953 6 0.68%

Oil 65.08 -0.32 -0.49%

Today's economic calendar:

Jobless Claims 8:30 AM ET

Existing Home Sales 10:00 AM ET

EIA Natural Gas Report 10:30 AM ET

3-Month Bill Announcement 11:00 AM ET

6-Month Bill Announcement 11:00 AM ET

52-Week Bill Announcement 11:00 AM ET

2-Yr Note Announcement 11:00 AM ET

5-Yr Note Announcement 11:00 AM ET

7-Yr Note Announcement 11:00 AM ET

20-Yr TIPS Announcement 11:00 AM ET

Money Supply 4:30 PM ET

Today's earnings reports:

There are over 240 reporting today - too many to list.

Wednesday, July 22, 2009

CNBC takes on the Bloggers - again - Charlie Gasparino and MCC - 2:45

Funny stuff here. They are talking about Zero Hedge, one of the best blogs on the net.

This is the third or forth time CNBC has ripped the bloggers. Maybe we wouldn't turn to blogger if CNBC actually gave us some worthwhile news.

NEWSFLASH TO CNBC - Investors/traders want substance, not relentless pumping and ass kissing of the Wall Street elite.

Lunchtime reading - 11:55AM

Morgan Stanley Sets Aside 72% of Revenue for Employees’ Pay - Bloomberg

CIT Hit With Interest Rate More Than 25 Times Libor (Update2) - Bloomberg

Wells Fargo’s Bad Loans Rise in Quarter; Shares Drop (Update2) - Bloomberg

Morgan Stanley Loss Misses Estimates on Debt Costs (Update2) - Bloomberg

Week-to-week mortgage filings up 2.8% as rates rise: MBA - MarketWatch

Whirlpool shares off 10% as profit falls on weaker demand - MarketWatch

Apple smashes profit forecasts, iPhone shines - Reuters

Pre-market - July 22, 2009

Futures down a little this morning:

DJIA INDEX 8,851.00 -35.00

S&P 500 950.50 -2.90 951.20

NASDAQ 100 1,554.00 0.00

Gold 947 -2 -0.20%

Oil 65.02 -0.59 -0.90%

Today's economic calendar:

MBA Purchase Applications 7:00 AM ET

Ben Bernanke Speaks 10:00 AM ET

EIA Petroleum Status Report 10:30 AM ET

Today's earnings calendar:

Before market opens

Before market opens

Today after close

Today after close

Before market opens

Before market opens

Today after close

Today after close

Tuesday, July 21, 2009

Market wrap - 4:15PM

The market didn't see the CAT earnings quite as good as CNBC. The stock traded lower for the day after a large run up pre-market. All indexes were down most of the morning due to dollar weakness and the Bernanke testimony. Around 1:00 or a little after the steady climb upward, to close at:

Dow 8,915.19 +67.04 (0.76%)

S&P 500 954.54 +3.41 (0.36%)

Nasdaq 1,916.20 +6.91 (0.36%)

Gold 947 -2 -0.20%

Oil 64.72 +0.74 +1.16%

Today by sector:

Today's heatmap:

Today's heatmap:

After the bell earnings - AAPL, AMD,SBUX,YHOO

Today's heatmap:

After the bell earnings - AAPL, AMD,SBUX,YHOO

Neil Barosfky - TARP - CNBC - The truth is here somewhere - 10:35AM

Full report can be found here. I didn't link the document, it is very long. Look or the link called - July 21, 2009 - Quarterly Report to Congress [PDF]

This was all over yesterday, but the document was not available. Now it is. Of course the cheerleaders on CNBC had the guy on this morning, which as usual, they botched up like they normally would. What a pathetic bunch they are.

Video here:

Read the report, don't believe these ass clowns.

Bernanke article in the WSJ - 9:10AM

The Fed’s Exit Strategy - WSJ

By BEN BERNANKE

The depth and breadth of the global recession has required a highly accommodative monetary policy. Since the onset of the financial crisis nearly two years ago, the Federal Reserve has reduced the interest-rate target for overnight lending between banks (the federal-funds rate) nearly to zero. We have also greatly expanded the size of the Fed’s balance sheet through purchases of longer-term securities and through targeted lending programs aimed at restarting the flow of credit.

These actions have softened the economic impact of the financial crisis. They have also improved the functioning of key credit markets, including the markets for interbank lending, commercial paper, consumer and small-business credit, and residential mortgages.

My colleagues and I believe that accommodative policies will likely be warranted for an extended period. At some point, however, as economic recovery takes hold, we will need to tighten monetary policy to prevent the emergence of an inflation problem down the road. The Federal Open Market Committee, which is responsible for setting U.S. monetary policy, has devoted considerable time to issues relating to an exit strategy. We are confident we have the necessary tools to withdraw policy accommodation, when that becomes appropriate, in a smooth and timely manner.

View Full Image

Chad Crowe

The exit strategy is closely tied to the management of the Federal Reserve balance sheet. When the Fed makes loans or acquires securities, the funds enter the banking system and ultimately appear in the reserve accounts held at the Fed by banks and other depository institutions. These reserve balances now total about $800 billion, much more than normal. And given the current economic conditions, banks have generally held their reserves as balances at the Fed.

But as the economy recovers, banks should find more opportunities to lend out their reserves. That would produce faster growth in broad money (for example, M1 or M2) and easier credit conditions, which could ultimately result in inflationary pressures—unless we adopt countervailing policy measures. When the time comes to tighten monetary policy, we must either eliminate these large reserve balances or, if they remain, neutralize any potential undesired effects on the economy.

To some extent, reserves held by banks at the Fed will contract automatically, as improving financial conditions lead to reduced use of our short-term lending facilities, and ultimately to their wind down. Indeed, short-term credit extended by the Fed to financial institutions and other market participants has already fallen to less than $600 billion as of mid-July from about $1.5 trillion at the end of 2008. In addition, reserves could be reduced by about $100 billion to $200 billion each year over the next few years as securities held by the Fed mature or are prepaid. However, reserves likely would remain quite high for several years unless additional policies are undertaken.

Even if our balance sheet stays large for a while, we have two broad means of tightening monetary policy at the appropriate time: paying interest on reserve balances and taking various actions that reduce the stock of reserves. We could use either of these approaches alone; however, to ensure effectiveness, we likely would use both in combination.

Congress granted us authority last fall to pay interest on balances held by banks at the Fed. Currently, we pay banks an interest rate of 0.25%. When the time comes to tighten policy, we can raise the rate paid on reserve balances as we increase our target for the federal funds rate.

Banks generally will not lend funds in the money market at an interest rate lower than the rate they can earn risk-free at the Federal Reserve. Moreover, they should compete to borrow any funds that are offered in private markets at rates below the interest rate on reserve balances because, by so doing, they can earn a spread without risk.

Thus the interest rate that the Fed pays should tend to put a floor under short-term market rates, including our policy target, the federal-funds rate. Raising the rate paid on reserve balances also discourages excessive growth in money or credit, because banks will not want to lend out their reserves at rates below what they can earn at the Fed.

Considerable international experience suggests that paying interest on reserves effectively manages short-term market rates. For example, the European Central Bank allows banks to place excess reserves in an interest-paying deposit facility. Even as that central bank’s liquidity-operations substantially increased its balance sheet, the overnight interbank rate remained at or above its deposit rate. In addition, the Bank of Japan and the Bank of Canada have also used their ability to pay interest on reserves to maintain a floor under short-term market rates.

Despite this logic and experience, the federal-funds rate has dipped somewhat below the rate paid by the Fed, especially in October and November 2008, when the Fed first began to pay interest on reserves. This pattern partly reflected temporary factors, such as banks’ inexperience with the new system.

However, this pattern appears also to have resulted from the fact that some large lenders in the federal-funds market, notably government-sponsored enterprises such as Fannie Mae and Freddie Mac, are ineligible to receive interest on balances held at the Fed, and thus they have an incentive to lend in that market at rates below what the Fed pays banks.

Under more normal financial conditions, the willingness of banks to engage in the simple arbitrage noted above will tend to limit the gap between the federal-funds rate and the rate the Fed pays on reserves. If that gap persists, the problem can be addressed by supplementing payment of interest on reserves with steps to reduce reserves and drain excess liquidity from markets—the second means of tightening monetary policy. Here are four options for doing this.

First, the Federal Reserve could drain bank reserves and reduce the excess liquidity at other institutions by arranging large-scale reverse repurchase agreements with financial market participants, including banks, government-sponsored enterprises and other institutions. Reverse repurchase agreements involve the sale by the Fed of securities from its portfolio with an agreement to buy the securities back at a slightly higher price at a later date.

Second, the Treasury could sell bills and deposit the proceeds with the Federal Reserve. When purchasers pay for the securities, the Treasury’s account at the Federal Reserve rises and reserve balances decline.

The Treasury has been conducting such operations since last fall under its Supplementary Financing Program. Although the Treasury’s operations are helpful, to protect the independence of monetary policy, we must take care to ensure that we can achieve our policy objectives without reliance on the Treasury.

Third, using the authority Congress gave us to pay interest on banks’ balances at the Fed, we can offer term deposits to banks—analogous to the certificates of deposit that banks offer their customers. Bank funds held in term deposits at the Fed would not be available for the federal funds market.

Fourth, if necessary, the Fed could reduce reserves by selling a portion of its holdings of long-term securities into the open market.

Each of these policies would help to raise short-term interest rates and limit the growth of broad measures of money and credit, thereby tightening monetary policy.

Overall, the Federal Reserve has many effective tools to tighten monetary policy when the economic outlook requires us to do so. As my colleagues and I have stated, however, economic conditions are not likely to warrant tighter monetary policy for an extended period. We will calibrate the timing and pace of any future tightening, together with the mix of tools to best foster our dual objectives of maximum employment and price stability.

—Mr. Bernanke is chairman of the Federal Reserve.

Pre - market - July 21, 2009AM

Futures up this morning after CAT came out with better than expected earnings:

DJIA INDEX 8,838.00 33.00

S&P 500 952.20 3.20 947.60

NASDAQ 100 1,545.25 4.75

Gold 949 11 1.21%

Oil 64.39 0.41 0.64%

Today's economic calendar:

ICSC-Goldman Store Sales 7:45 AM ET

Redbook 8:55 AM ET

Bank of Canada Announcement 9:00 AM ET

Ben Bernanke Speaks 10:00 AM ET

4-Week Bill Auction 1:00 PM ET

Today's earnings reports:

Before market opens

Before market opens

After market closes

After market closes

Before market opens

Before market opens

After market closes

After market closes

Monday, July 20, 2009

Market wrap - 4:15PM

This rocketship of a market continues, on no volume of course. But maybe the upgrade from Goldman Sachs this morning had something to do with it.

Dow 8,847.93 +103.99 (1.19%)

S&P 500 950.97 +10.59 (1.13%)

Nasdaq 1,909.29 +22.68 (1.20%)

Gold 949 +11 +1.21%

Oil 64.33 0.42 0.66%

Today by sector:

Today's heatmap:

Today's heatmap:

Tomorrow morning earnings:

Tomorrow morning earnings:

Any minute now, CNBC will have Nouriel Roubini on to explain his call last week "the recession will end by the end of the year" that CNBC made, which drove the marke up that day. Roubini later came out and said he never said that. In case you are not familiar with Roubini, he is known as Dr. Doom, for forecasting this crisis back in 2006. He has been mocked repeatedly by CNBC over the last year, and quite often and increasingly worse in the last few months. The new main pumper of Fast Money, Joe "buy everything in sight" Terranova took another shot at him today when he said something to the effect "I am long whatever Roubini is short" or something like that. Screw you Joe, you have the credibility of a turd. I will post the interview if they put in on their website. Watch for the earnings reports from Texas Instruments after the bell today. The spin doctors will use this tonight and tomorrow to pump this bullshit market even higher - if anyone other than Goldman Sachs is trading it.

Today's heatmap:

Tomorrow morning earnings:

Any minute now, CNBC will have Nouriel Roubini on to explain his call last week "the recession will end by the end of the year" that CNBC made, which drove the marke up that day. Roubini later came out and said he never said that. In case you are not familiar with Roubini, he is known as Dr. Doom, for forecasting this crisis back in 2006. He has been mocked repeatedly by CNBC over the last year, and quite often and increasingly worse in the last few months. The new main pumper of Fast Money, Joe "buy everything in sight" Terranova took another shot at him today when he said something to the effect "I am long whatever Roubini is short" or something like that. Screw you Joe, you have the credibility of a turd. I will post the interview if they put in on their website. Watch for the earnings reports from Texas Instruments after the bell today. The spin doctors will use this tonight and tomorrow to pump this bullshit market even higher - if anyone other than Goldman Sachs is trading it.

Goldman Ups S&P 500 Target for End-Year - 9:07AM

Goldman Ups S&P 500 Target for End-Year - CNBC (sorry to send you there)

Goldman Sachs raised the S&P 500 index's target for the end of the year to 1060 from 940 Monday, but said the risk of "double-dip" recession remains significant.

Goldman Sachs made the move to reflect potential price return of about 13 percent from the current levels, Reuters reported.

It also raised the S&P 500 operating earnings view to $52 from $40 for this year.

Operating earnings view for next year was also raised to $75 from $63.

Goldman's current economic view is for below-trend growth through 2010, and it believes the risk of a "double-dip" recession is still significant.

Asian markets rallied, with the Hang Seng index closing more than 3.7 percent up, while European stock indexes were also up, with banks dominating the upturn.

Stock markets in the US and Europe are likely to see a significant rally if indexes manage to rise further from current levels, technical analyst Clem Chambers, CEO of ADVFN, also said Monday.

© 2009 CNBC.com

Really! Goldman Sachs - upgrading the price target of the S&P - sound familiar? Oil, other banks, etc? At this point, I don't believe anything these people say.

Really! Goldman Sachs - upgrading the price target of the S&P - sound familiar? Oil, other banks, etc? At this point, I don't believe anything these people say.

Pre-market - July 20, 2009 - 8:10AM

Futures up this morning on news that CIT will be bailed out:

DJIA INDEX 8,753.00 56.00

S&P 500 943.20 6.30 936.90

NASDAQ 100 1,535.50 7.50

Gold 938 2 0.22%

Oil 64.66 +1.10 +1.73%

Today's economic calendar:

Leading Indicators 10:00 AM ET

4-Week Bill Announcement 11:00 AM ET

3-Month Bill Auction 1:00 PM ET

6-Month Bill Auction 1:00 PM ET

Today's earnings reports:

Before market opens

Before market opens

Today after close

Today after close

Before market opens

Before market opens

Today after close

Today after close

Subscribe to:

Comments (Atom)