Full report here

UNEMPLOYMENT INSURANCE WEEKLY CLAIMS REPORT

SEASONALLY ADJUSTED DATA

In the week ending Oct. 24, the advance figure for seasonally adjusted initial claims was 530,000, a decrease of 1,000 from the previous week's unrevised figure of 531,000. The 4-week moving average was 526,250, a decrease of 6,000 from the previous week's unrevised average of 532,250.

The advance seasonally adjusted insured unemployment rate was 4.4 percent for the week ending Oct. 17, a decrease of 0.1 percentage point from the prior week's unrevised rate of 4.5 percent.

The advance number for seasonally adjusted insured unemployment during the week ending Oct. 17 was 5,797,000, a decrease of 148,000 from the preceding week's revised level of 5,945,000. The 4-week moving average was 5,960,750, a decrease of 78,750 from the preceding week's revised average of 6,039,500.

UNADJUSTED DATA

The advance number of actual initial claims under state programs, unadjusted, totaled 492,456 in the week ending Oct. 24, an increase of 32,026 from the previous week. There were 449,389 initial claims in the comparable week in 2008.

The advance unadjusted insured unemployment rate was 3.8 percent during the week ending Oct. 17, an increase of 0.1 percentage point from the prior week. The advance unadjusted number for persons claiming UI benefits in state programs totaled 4,968,019, an increase of 51,445 from the preceding week. A year earlier, the rate was 2.4 percent and the volume was 3,233,118.

Extended benefits were available in Alabama, Alaska, Arizona, California, Colorado, Connecticut, Delaware, the District of Columbia, Florida, Georgia, Idaho, Illinois, Indiana, Kansas, Kentucky, Maine, Massachusetts, Michigan, Minnesota, Missouri, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Oregon, Pennsylvania, Puerto Rico, Rhode Island, South Carolina, Tennessee, Texas, Vermont, Virginia, Washington, West Virginia, and Wisconsin during the week ending Oct. 10.

Initial claims for UI benefits by former Federal civilian employees totaled 1,895 in the week ending Oct. 17, a decrease of 337 from the prior week. There were 2,417 initial claims by newly discharged veterans, a decrease of 231 from the preceding week.

There were 21,217 former Federal civilian employees claiming UI benefits for the week ending Oct. 10, an increase of 1,096 from the previous week. Newly discharged veterans claiming benefits totaled 33,081, an increase of 2,343 from the prior week.

States reported 3,368,909 persons claiming EUC (Emergency Unemployment Compensation) benefits for the week ending Oct. 10, a decrease of 21,713 from the prior week. There were 1,050,369 claimants in the comparable week in 2008. EUC weekly claims include both first and second tier activity.

The highest insured unemployment rates in the week ending Oct. 10 were in Puerto Rico (6.3 percent), Nevada (5.3), Oregon (5.3), Pennsylvania (5.0), Wisconsin (4.8), Arkansas (4.6), California (4.6), Michigan (4.6), North Carolina (4.5), and South Carolina (4.5).

The largest increases in initial claims for the week ending Oct. 17 were in California (+5,774), Puerto Rico (+685), Minnesota (+614), Nevada (+366), and Nebraska (+239), while the largest decreases were in Wisconsin (-5,681), New York (-4,711), Pennsylvania (-4,033), Illinois (-3,870), and Oregon

(-2,706).

More at link with formatted tables

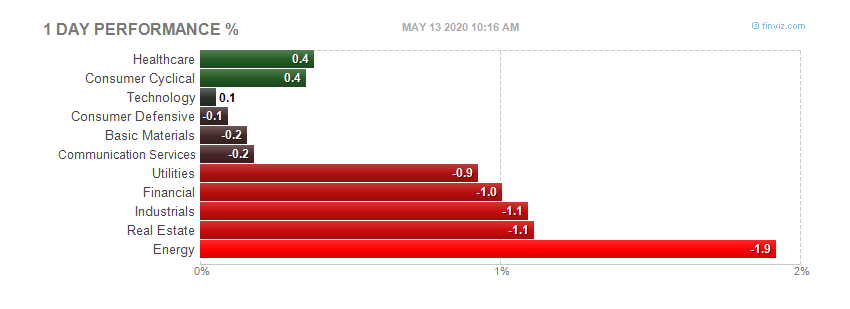

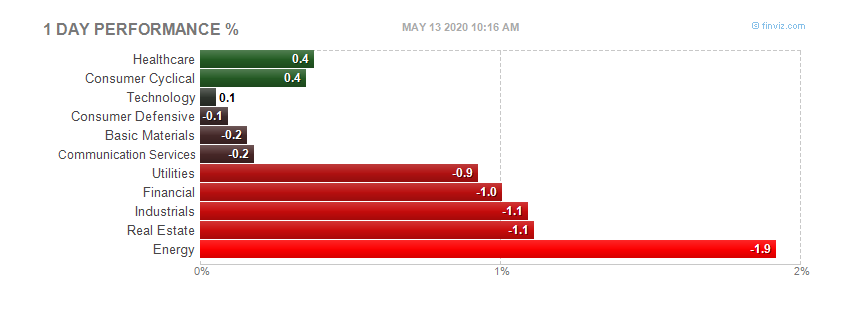

Today's heatmap:

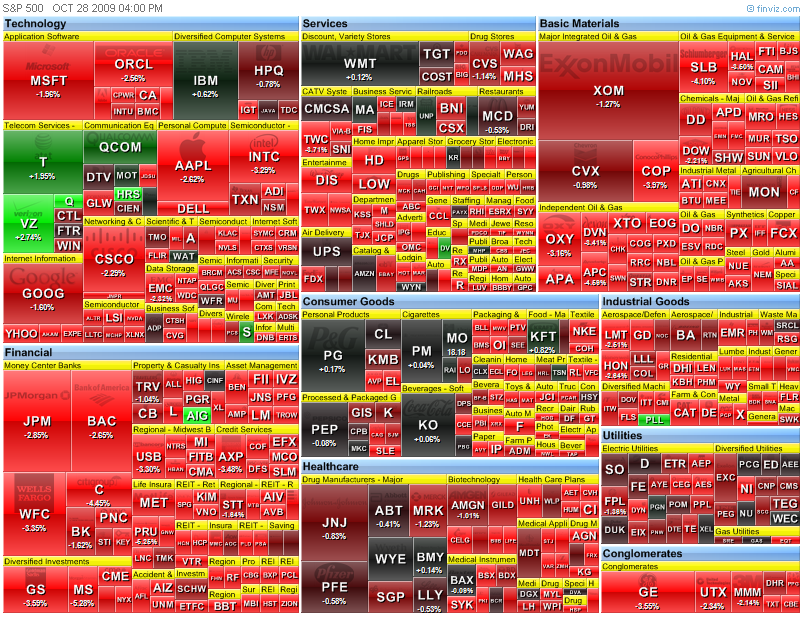

Today's heatmap:

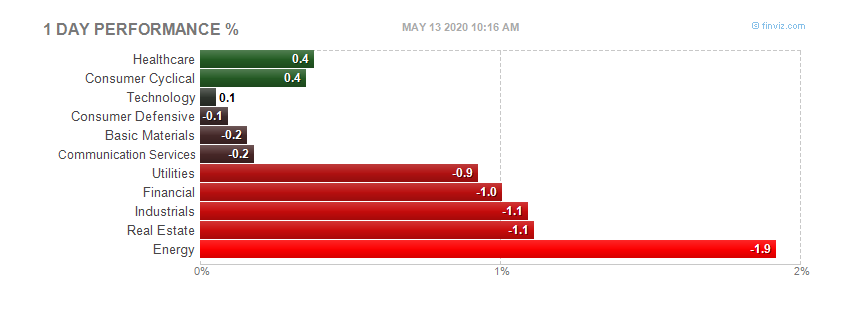

Today's heatmap:

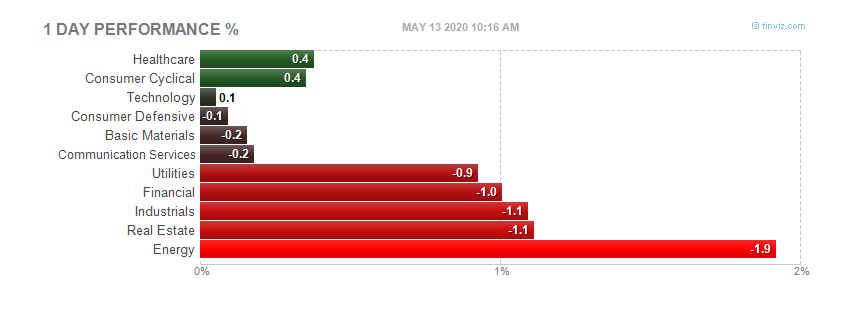

Today's heatmap:

Investor Confidence Index Declines from 122.8 to 118.1 in September

29/09/2009

Boston, September 29, 2009 – State Street Global Markets, the investment research and trading arm of State Street Corporation (NYSE:STT), today released the results of the State Street Investor Confidence Index® for September 2009.

Global Investor Confidence fell by 4.7 points to 118.1 from a revised August level of 122.8. Regionally, there was some divergence in risk appetite. The confidence of North American institutional investors declined slightly by 4.6 points from 118.3 to 113.7. Elsewhere, however, the tone was more upbeat. European Investor Confidence rose from a revised 109.3 to 110.9, while Asian Investor Confidence increased from a revised 91.9 to 93.1.

Developed through State Street Global Markets’ research partnership, State Street Associates, by Harvard University professor Ken Froot and State Street Associates Director Paul O’Connell, the State Street Investor Confidence Index measures investor confidence on a quantitative basis by analyzing the actual buying and selling patterns of institutional investors. The index is based on financial theory that assigns precise meaning to changes in investor risk appetite, or the willingness of investors to allocate their portfolios to equities. The more of their portfolio that institutional investors are willing to devote to equities, the greater their risk appetite or confidence.

“After eight consecutive increases in Global Investor Confidence, which took the Index from an all-time low of 82.1 during the financial crisis to a five-year high of 122.8, institutional investors took a breather this month and consolidated their holdings of risky assets,” commented Froot. “This month's reading of 118.1 is still comfortably in the range associated with the accumulation of risk exposures, as a reading of 100 signifies neither accumulation nor decumulation. However, there is a recognition that a portion of the recent rise in global equity prices can be attributed to liquidity expansion rather than fundamental opportunities. Institutional investors are pausing to assess this balance.”

“The regional variation that we noted last month has continued into this month,” added O’Connell. “During the financial crisis and the subsequent recovery, European investor risk appetite has lagged that of North American institutions by about three months. This month, the European Confidence Index registered its sixth consecutive monthly increase, but the rate of increase has slowed. As is true of North American investors, European and Asian institutions will be weighing the prospects for long-term improvement in fundamentals against the eventual withdrawal of the ample liquidity currently being provided by policy makers.”

Investor Confidence Index Declines from 122.8 to 118.1 in September

29/09/2009

Boston, September 29, 2009 – State Street Global Markets, the investment research and trading arm of State Street Corporation (NYSE:STT), today released the results of the State Street Investor Confidence Index® for September 2009.

Global Investor Confidence fell by 4.7 points to 118.1 from a revised August level of 122.8. Regionally, there was some divergence in risk appetite. The confidence of North American institutional investors declined slightly by 4.6 points from 118.3 to 113.7. Elsewhere, however, the tone was more upbeat. European Investor Confidence rose from a revised 109.3 to 110.9, while Asian Investor Confidence increased from a revised 91.9 to 93.1.

Developed through State Street Global Markets’ research partnership, State Street Associates, by Harvard University professor Ken Froot and State Street Associates Director Paul O’Connell, the State Street Investor Confidence Index measures investor confidence on a quantitative basis by analyzing the actual buying and selling patterns of institutional investors. The index is based on financial theory that assigns precise meaning to changes in investor risk appetite, or the willingness of investors to allocate their portfolios to equities. The more of their portfolio that institutional investors are willing to devote to equities, the greater their risk appetite or confidence.

“After eight consecutive increases in Global Investor Confidence, which took the Index from an all-time low of 82.1 during the financial crisis to a five-year high of 122.8, institutional investors took a breather this month and consolidated their holdings of risky assets,” commented Froot. “This month's reading of 118.1 is still comfortably in the range associated with the accumulation of risk exposures, as a reading of 100 signifies neither accumulation nor decumulation. However, there is a recognition that a portion of the recent rise in global equity prices can be attributed to liquidity expansion rather than fundamental opportunities. Institutional investors are pausing to assess this balance.”

“The regional variation that we noted last month has continued into this month,” added O’Connell. “During the financial crisis and the subsequent recovery, European investor risk appetite has lagged that of North American institutions by about three months. This month, the European Confidence Index registered its sixth consecutive monthly increase, but the rate of increase has slowed. As is true of North American investors, European and Asian institutions will be weighing the prospects for long-term improvement in fundamentals against the eventual withdrawal of the ample liquidity currently being provided by policy makers.”

Full report hereThe Conference Board Consumer Confidence Index® Declines in October

October 27, 2009

The Conference Board Consumer Confidence Index®, which had declined in September, deteriorated further in October. The Index now stands at 47.7 (1985=100), down from 53.4 in September. The Present Situation Index decreased to 20.7 from 23.0 last month. The Expectations Index declined to 65.7 from 73.7 in September.

The Consumer Confidence Survey® is based on a representative sample of 5,000 U.S. households. The monthly survey is conducted for The Conference Board by TNS. TNS is the world's largest custom research company. The cutoff date for October's preliminary results was October 21st.

Says Lynn Franco, Director of The Conference Board Consumer Research Center: "Consumers' assessment of present-day conditions has grown less favorable, with labor market conditions playing a major role in this grimmer assessment. In fact, the Present Situation Index is now at its lowest reading in 26 years (Index 17.5, Feb. 1983). The short-term outlook has also grown more negative, as a greater proportion of consumers anticipate business and labor market conditions will worsen in the months ahead. Consumers also remain quite pessimistic about their future earnings, a sentiment that will likely constrain spending during the holidays."

Consumers' assessment of current conditions worsened in October. Those claiming business conditions are "bad" increased to 47.1 percent from 46.3 percent, while those claiming conditions are "good" decreased to 7.7 percent from 8.6 percent. Consumers' appraisal of the labor market was also bleaker. Those claiming jobs are "hard to get" increased to 49.6 percent from 47.0 percent, while those claiming jobs are "plentiful" decreased to 3.4 percent from 3.6 percent.

Consumers' short-term outlook grew more pessimistic in October. Those anticipating an improvement in business conditions over the next six months decreased to 20.8 percent from 21.3 percent, while those expecting conditions to worsen increased to 18.3 percent from 14.6 percent.

The labor market outlook was also more negative. The percentage of consumers expecting more jobs in the months ahead declined to 16.3 percent from 18.0 percent, while those expecting fewer jobs increased to 26.6 percent from 22.9 percent. The proportion of consumers expecting an increase in their incomes decreased to 10.3 percent from 11.2 percent.

Full report hereThe Conference Board Consumer Confidence Index® Declines in October

October 27, 2009

The Conference Board Consumer Confidence Index®, which had declined in September, deteriorated further in October. The Index now stands at 47.7 (1985=100), down from 53.4 in September. The Present Situation Index decreased to 20.7 from 23.0 last month. The Expectations Index declined to 65.7 from 73.7 in September.

The Consumer Confidence Survey® is based on a representative sample of 5,000 U.S. households. The monthly survey is conducted for The Conference Board by TNS. TNS is the world's largest custom research company. The cutoff date for October's preliminary results was October 21st.

Says Lynn Franco, Director of The Conference Board Consumer Research Center: "Consumers' assessment of present-day conditions has grown less favorable, with labor market conditions playing a major role in this grimmer assessment. In fact, the Present Situation Index is now at its lowest reading in 26 years (Index 17.5, Feb. 1983). The short-term outlook has also grown more negative, as a greater proportion of consumers anticipate business and labor market conditions will worsen in the months ahead. Consumers also remain quite pessimistic about their future earnings, a sentiment that will likely constrain spending during the holidays."

Consumers' assessment of current conditions worsened in October. Those claiming business conditions are "bad" increased to 47.1 percent from 46.3 percent, while those claiming conditions are "good" decreased to 7.7 percent from 8.6 percent. Consumers' appraisal of the labor market was also bleaker. Those claiming jobs are "hard to get" increased to 49.6 percent from 47.0 percent, while those claiming jobs are "plentiful" decreased to 3.4 percent from 3.6 percent.

Consumers' short-term outlook grew more pessimistic in October. Those anticipating an improvement in business conditions over the next six months decreased to 20.8 percent from 21.3 percent, while those expecting conditions to worsen increased to 18.3 percent from 14.6 percent.

The labor market outlook was also more negative. The percentage of consumers expecting more jobs in the months ahead declined to 16.3 percent from 18.0 percent, while those expecting fewer jobs increased to 26.6 percent from 22.9 percent. The proportion of consumers expecting an increase in their incomes decreased to 10.3 percent from 11.2 percent.

Today's heatmap:

Today's heatmap: