Friday, September 4, 2009

Employment report - 8:30am

Not so good - full report here

Transmission of material in this release is embargoed until 8:30 a.m. (EDT) September 4, 2009

THE EMPLOYMENT SITUATION -- AUGUST 2009

Nonfarm payroll employment continued to decline in August (-216,000),

and the unemployment rate rose to 9.7 percent, the U.S. Bureau of Labor

Statistics reported today. Although job losses continued in many of the

major industry sectors in August, the declines have moderated in recent

months.

Household Survey Data

In August, the number of unemployed persons increased by 466,000 to 14.9

million, and the unemployment rate rose by 0.3 percentage point to 9.7

percent. The rate had been little changed in June and July, after in-

creasing 0.4 or 0.5 percentage point in each month from December 2008

through May. Since the recession began in December 2007, the number of

unemployed persons has risen by 7.4 million, and the unemployment rate

has grown by 4.8 percentage points. (See table A-1.)

Among the major worker groups, the unemployment rates for adult men

(10.1 percent), whites (8.9 percent), and Hispanics (13.0 percent) rose

in August. The jobless rates for adult women (7.6 percent), teenagers

(25.5 percent), and blacks (15.1 percent) were little changed over the

month. The unemployment rate for Asians was 7.5 percent, not seasonally

adjusted. (See tables A-1, A-2, and A-3.)

The civilian labor force participation rate remained at 65.5 percent in

August. The employment-population ratio, at 59.2 percent, edged down

over the month and has declined by 3.5 percentage points since the re-

cession began in December 2007. (See table A-1.)

In August, the number of persons working part time for economic reasons

was little changed at 9.1 million. These individuals indicated that they

were working part time because their hours had been cut back or because

they were unable to find a full-time job. The number of such workers

rose sharply in the fall and winter but has been little changed since

March. (See table A-5.)

About 2.3 million persons were marginally attached to the labor force

in August, reflecting an increase of 630,000 from a year earlier. (The

data are not seasonally adjusted.) These individuals were not in the

labor force, wanted and were available for work, and had looked for a

job sometime in the prior 12 months. They were not counted as unemployed

because they had not searched for work in the 4 weeks preceding the sur-

vey. (See table A-13.)

Among the marginally attached, the number of discouraged workers in

August (758,000) has nearly doubled over the past 12 months. (The data

are not seasonally adjusted.) Discouraged workers are persons not cur-

rently looking for work because they believe no jobs are available for

them. The other 1.5 million persons marginally attached to the labor

force in August had not searched for work in the 4 weeks preceding the

survey for reasons such as school attendance or family responsibilities.

Establishment Survey Data

Total nonfarm payroll employment declined by 216,000 in August. Since

December 2007, employment has fallen by 6.9 million. In recent months,

job losses have moderated in many major industry sectors. (See table

B-1.)

In August, construction employment declined by 65,000, in line with

the trend since May. Monthly losses had averaged 117,000 over the 6

months ending in April. Employment in the construction industry has

contracted by 1.4 million since the onset of the recession. Starting

in early 2009, the larger share of monthly job losses shifted from the

residential to the nonresidential and heavy construction components.

In mining, employment declined by 9,000 over the month.

In August, manufacturing employment continued to trend downward, with

a decline of 63,000. The pace of job loss has slowed throughout manu-

facturing in recent months. Motor vehicles and parts lost 15,000 jobs

in August, partly offsetting a 31,000 employment increase in July.

Financial activities shed 28,000 jobs in August, with declines spread

throughout the industry. Job loss in financial activities has slowed

since the beginning of the year. Employment in the industry has de-

clined by 537,000 since the start of the recession.

Wholesale trade employment fell by 17,000 in August. Employment in

information continued to trend down over the month.

Employment in the retail trade industry was little changed in August.

Employment also was little changed in professional and business ser-

vices over the month. From May through August, monthly employment

declines in the sector averaged 46,000, compared with 138,000 per

month from November through April. Job loss in its temporary help

services component has slowed markedly over the last 4 months.

Employment was little changed in August both in transportation and

warehousing, and in leisure and hospitality.

Employment in health care continued to rise in August (28,000), with

gains in ambulatory care and in nursing and residential care. Employ-

ment in hospitals was little changed in August; job growth in the

industry slowed in early 2009 and employment has been flat since May.

Health care has added 544,000 jobs since the start of the recession.

In August, the average workweek for production and nonsupervisory

workers on private nonfarm payrolls was unchanged at 33.1 hours.

The manufacturing workweek and factory overtime also showed no

change over the month (at 39.8 hours and 2.9 hours, respectively).

(See table B-2.)

In August, average hourly earnings of production and nonsupervisory

workers on private nonfarm payrolls rose by 6 cents, or 0.3 percent,

to $18.65. Over the past 12 months, average hourly earnings have risen

by 2.6 percent, while average weekly earnings have risen by only 0.8

percent due to declines in the average workweek. (See table B-3.)

The change in total nonfarm payroll employment for June was revised

from -443,000 to -463,000, and the change for July was revised from

-247,000 to -276,000.

_____________

The Employment Situation for September is scheduled to be released on

Friday, October 2, 2009, at 8:30 a.m. (EDT).

More at link

Pre-market - Friday, September 4, 2009

Futures up slightly this morning waiting on the much awaited jobs report out at 8:30

DJIA INDEX 9,357.00 27.00

S&P 500 1,005.20 3.50

NASDAQ 100 1,611.25 7.25

Today's economic calendar:

Employment Situation 8:30 AM ET

Treasury STRIPS 3:00 PM ET

Today's earnings reports:

Before market opens:

DFZ RG Barry Corp. Consumer Goods Textile - Apparel Footwear & Accessories

HRB H&R Block, Inc. Services Personal Services

After close = none

Market wrap - Thursday - September 3, 2009

A pretty uneventful day in the market today.

Dow 9,344.61 +63.94 (0.69%)

S&P 500 1,003.24 +8.49 (0.85%)

Nasdaq 1,983.20 +16.13 (0.82%)

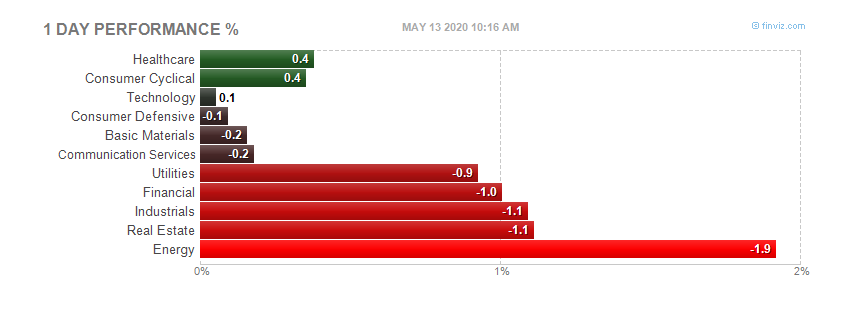

Today by sector(the banks win again).

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Thursday, September 3, 2009

ISM Non-manufacturing data - 10:am

Full report here

August 2009 Non-Manufacturing ISM Report On Business®

NMI (Non-Manufacturing Index) at 48.4%

DO NOT CONFUSE THIS NATIONAL REPORT with the various regional purchasing reports released across the country. The national report's information reflects the entire United States, while the regional reports contain primarily regional data from their local vicinities. Also, the information in the regional reports is not used in calculating the results of the national report. The information compiled in this report is for the month of August 2009.

Business Activity Index at 51.3%

New Orders Index at 49.9%

Employment Index at 43.5%

(Tempe, Arizona) — Economic activity in the non-manufacturing sector contracted in August, say the nation's purchasing and supply executives in the latest Non-Manufacturing ISM Report On Business®.

The report was issued today by Anthony Nieves, C.P.M., CFPM, chair of the Institute for Supply Management™ Non-Manufacturing Business Survey Committee; and senior vice president — supply management for Hilton Hotels Corporation. "The NMI (Non-Manufacturing Index) registered 48.4 percent in August, 2 percentage points higher than the 46.4 percent registered in July, indicating contraction in the non-manufacturing sector for the 11th consecutive month but at a slower rate. The Non-Manufacturing Business Activity Index increased 5.2 percentage points to 51.3 percent. This is the first time this index has reflected growth since September 2008. The New Orders Index increased 1.8 percentage points to 49.9 percent, and the Employment Index increased 2 percentage points to 43.5 percent. The Prices Index increased 21.8 percentage points to 63.1 percent in August, indicating a substantial increase in prices paid from July. According to the NMI, six non-manufacturing industries reported growth in August. Respondents' comments are mixed about business conditions and the overall economy; however, there is an increase in comments indicating that there are signs of improvement going forward."

INDUSTRY PERFORMANCE (Based on the NMI)

The six industries reporting growth in August based on the NMI composite index — listed in order — are: Real Estate, Rental & Leasing; Health Care & Social Assistance; Transportation & Warehousing; Utilities; Accommodation & Food Services; and Information. The 12 industries reporting contraction in August — listed in order — are: Management of Companies & Support Services; Mining; Finance & Insurance; Arts, Entertainment & Recreation; Professional, Scientific & Technical Services; Construction; Other Services; Agriculture, Forestry, Fishing & Hunting; Wholesale Trade; Educational Services; Public Administration; and Retail Trade.

WHAT RESPONDENTS ARE SAYING ...

* "While there are promising signs in the economy pointing toward the beginnings of a recovery, the financial services industry continues to be significantly affected by the downturn. Expectations are that the pace will begin to change by Q4 '09." (Finance & Insurance)

* "Business is still soft due to overall economic conditions." (Wholesale Trade)

* "There seems to be a more positive feeling about the economy." (Educational Services)

* "Healthcare reform still has hospitals wondering how they are going to get paid at the end of the day." (Health Care & Social Assistance)

* "Occupancy shows continued strength for the summer season, still below previous years' averages by 15% to 25%." (Accommodation & Food Services)

* "Business steady — revenue down slightly; however, less than expected." (Arts, Entertainment & Recreation)

* "Good first half results. Some evidence of consumers 'trading down.' Supplier lead times are very short." (Agriculture, Forestry, Fishing & Hunting)

More at link with formatted tables

Jobless claims - 8:30am

Full report here

UNEMPLOYMENT INSURANCE WEEKLY CLAIMS REPORT

SEASONALLY ADJUSTED DATA

In the week ending Aug. 22, the advance figure for seasonally adjusted initial claims was 570,000, a decrease of 10,000 from the previous week's revised figure of 580,000. The 4-week moving average was 566,250, a decrease of 4,750 from the previous week's revised average of 571,000.

The advance seasonally adjusted insured unemployment rate was 4.6 percent for the week ending Aug. 15, a decrease of 0.1 percentage point from the prior week's unrevised rate of 4.7 percent.

The advance number for seasonally adjusted insured unemployment during the week ending Aug. 15 was 6,133,000, a decrease of 119,000 from the preceding week's revised level of 6,252,000. The 4-week moving average was 6,241,750, a decrease of 27,000 from the preceding week's revised average of 6,268,750.

The fiscal year-to-date average for seasonally adjusted insured unemployment for all programs is 5.583 million.

UNADJUSTED DATA

The advance number of actual initial claims under state programs, unadjusted, totaled 453,936 in the week ending Aug. 22, a decrease of 4,049 from the previous week. There were 345,127 initial claims in the comparable week in 2008.

The advance unadjusted insured unemployment rate was 4.3 percent during the week ending Aug. 15, a decrease of 0.1 percentage point from the prior week. The advance unadjusted number for persons claiming UI benefits in state programs totaled 5,673,467, a decrease of 135,105 from the preceding week. A year earlier, the rate was 2.4 percent and the volume was 3,175,006.

Extended benefits were available in Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, the District of Columbia, Florida, Georgia, Idaho, Illinois, Indiana, Kansas, Kentucky, Maine, Massachusetts, Michigan, Minnesota, Missouri, Nevada, New Hampshire, New Jersey, New York, North Carolina, Ohio, Oregon, Pennsylvania, Puerto Rico, Rhode Island, South Carolina, Tennessee, Texas, Vermont, Virginia, Washington, West Virginia, and Wisconsin during the week ending Aug. 8.

Initial claims for UI benefits by former Federal civilian employees totaled 1,377 in the week ending Aug. 15, a decrease of 262 from the prior week. There were 2,054 initial claims by newly discharged veterans, a decrease of 198 from the preceding week.

There were 19,783 former Federal civilian employees claiming UI benefits for the week ending Aug. 8, a decrease of 794 from the previous week. Newly discharged veterans claiming benefits totaled 30,541, an increase of 216 from the prior week.

States reported 2,916,148 persons claiming EUC (Emergency Unemployment Compensation) benefits for the week ending Aug. 8, an increase of 38,392 from the prior week. There were 1,081,755 claimants in the comparable week in 2008. EUC weekly claims include both first and second tier activity.

The highest insured unemployment rates in the week ending Aug. 8 were in Puerto Rico (7.3 percent), Oregon (6.1), Pennsylvania (6.0), Michigan (5.9), Nevada (5.8), Wisconsin (5.5), California (5.4), Connecticut (5.4), New Jersey (5.2), North Carolina (5.0), and South Carolina (5.0).

The largest increases in initial claims for the week ending Aug. 15 were in Michigan (+4,068), Pennsylvania (+1,193), Florida (+1,148), Puerto Rico (+735), and Missouri (+649), while the largest decreases were in California (-6,286), Tennessee (-2,999), Texas (-2,557), Wisconsin (-2,075), and Ohio (-1,918).

More at link with formatted tables

Pre-market - September 3, 2009

Futures up slightly this morning waiting of the Jobless claims at 8:30:

DJIA INDEX 9,341.00 64.00

S&P 500 1,002.60 8.40

NASDAQ 100 1,606.00 13.00

Today's economic calendar:

Chain Store Sales

Monster Employment Index

ECB Announcement 7:45 AM ET

Jobless Claims 8:30 AM ET

RBC CASH Index 9:00 AM ET

30-Yr Bond Announcement 9:00 AM ET

ISM Non-Mfg Index 10:00 AM ET

EIA Natural Gas Report 10:30 AM ET

3-Month Bill Announcement 11:00 AM ET

6-Month Bill Announcement 11:00 AM ET

3-Yr Note Announcement 11:00 AM ET

10-Yr Note Announcement 11:00 AM ET

Today's earnings reports:

Before market opens

AHII Animal Health International, Inc. Services Medical Equipment Wholesale

CIEN CIENA Corp. Technology Communication Equipment

DLM Del Monte Foods Co. Consumer Goods Processed & Packaged Goods

FLOW Flow International Corp. Industrial Goods Machine Tools & Accessories

JTX Jackson Hewitt Tax Service Inc. Services Personal Services

LAYN Layne Christensen Co. Industrial Goods Heavy Construction

LTXC LTX-Credence Corporation Technology Semiconductor Equipment & Materials

MDZ MDS, Inc. Healthcare Specialized Health Services

MEI Methode Electronics Inc. Technology Diversified Electronics

MOV Movado Group Inc. Consumer Goods Recreational Goods, Other

NOVN Noven Pharmaceuticals Inc. Healthcare Drug Delivery

SCMR Sycamore Networks Inc. Technology Networking & Communication Devices

TK Teekay Corporation Services Shipping

UTIW UTI Worldwide, Inc. Services Air Delivery & Freight Services

After close

ARST ArcSight, Inc. Technology Business Software & Services

CHP C&D Technologies Inc. Technology Diversified Electronics

COO The Cooper Companies Inc. Healthcare Medical Instruments & Supplies

ESL Esterline Technologies Corp. Industrial Goods Aerospace/Defense Products & Services

FMCN Focus Media Holding Ltd. Services Advertising Agencies

GIII G-III Apparel Group, Ltd. Consumer Goods Textile - Apparel Clothing

PSEM Pericom Semiconductor Corp. Technology Semiconductor - Integrated Circuits

SNDA Shanda Interactive Entertainment Ltd. Technology Internet Software & Services

SWHC Smith & Wesson Holding Corp. Industrial Goods Aerospace/Defense Products & Services

TSCM TheStreet.com, Inc. Technology Internet Information Providers

ULTA Ulta Salon, Cosmetics & Fragrance, Inc. Services Personal Services

ZQK Quiksilver Inc. Consumer Goods Textile - Apparel Clothing

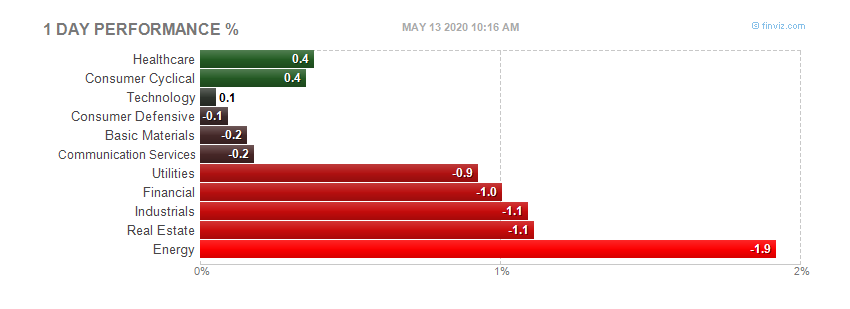

Market wrap for Wednesday - 8:00am

Not much movement today. Pretty boring actually:

Dow 9,280.67 -29.93 (-0.32%)

S&P 500 994.75 -3.29 (-0.33%)

Nasdaq 1,967.07 -1.82 (-0.09%)

Today by sector:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Wednesday, September 2, 2009

Factory orders - 10:00am

Full report here

HIGHLIGHTS FROM THE PRELIMINARY REPORT ON MANUFACTURERS' SHIPMENTS, INVENTORIES, AND ORDERS

July 2009 --------------- Released 10:00 A.M. EDT September 2, 2009

(M3-2(09)-07)

Note: All figures in text are in seasonally adjusted current dollars

For Data - (301) 763-4673

For Questions - Chris Savage or Jessica Young

(301) 763-4832

Summary

New orders for manufactured goods in July, up five of the last six months, increased $4.6 billion or 1.3 percent to $355.5 billion, the U.S. Census Bureau reported today. This followed a 0.9 percent June increase. Excluding transportation, new orders decreased 0.7 percent. Shipments, down eleven of the last twelve months, decreased $0.2 billion to $359.7 billion. This followed a 1.8 percent June increase. Unfilled orders, down ten consecutive months, decreased $0.1 billion to $740.6 billion. This was the longest streak of consecutive monthly decreases since the series was first published on a NAICS basis in 1992. This followed a 0.8 percent June decrease. The unfilled orders-to-shipments ratio was 5.95, down from 6.00 in June. Inventories, down eleven consecutive months, decreased $3.6 billion or 0.7 percent to $503.1 billion. This was the longest streak of consecutive monthly decreases since March 2003-January 2004 and followed a 1.1 percent June decrease. The inventories-to-shipments ratio was 1.40, down from 1.41 in June.

New Orders

New orders for manufactured durable goods in July, up three of the last four months, increased $8.2 billion or 5.1 percent to $169.0 billion, revised from the previously published 4.9 percent increase. This followed a 1.1 percent June decrease.

New orders for manufactured nondurable goods decreased $3.6 billion or 1.9 percent to $186.5 billion.

Shipments

Shipments of manufactured durable goods in July, up two consecutive months, increased $3.4 billion or 2.0 percent to $173.3 billion, unchanged from the previously published increase. This followed a 0.8 percent June increase.

Shipments of manufactured nondurable goods, down following two consecutive monthly increases, decreased $3.6 billion or 1.9 percent to $186.5 billion. This followed a 2.8 percent June increase. This decrease was led by petroleum and coal products, which decreased $2.7 billion or 7.2 percent to $34.3 billion.

Unfilled Orders

Unfilled orders for manufactured durable goods in July, down ten consecutive months, decreased $0.1 billion to $740.6 billion, revised from the previously published 0.1 percent decrease. This was the longest streak of consecutive monthly decreases since the series was first published on a NAICS basis in 1992 and followed a 0.8 percent June decrease.

Inventories

Inventories of manufactured durable goods in July, down seven consecutive months, decreased $2.9 billion or 0.9 percent to $313.7 billion, revised from the previously published 0.8 percent decrease. This followed a 1.5 percent June decrease.

Inventories of manufactured nondurable goods, down eleven consecutive months, decreased $0.7 billion or 0.4 percent to $189.4 billion. This followed a 0.4 percent June decrease. Plastic and rubber products led the decrease, down $0.4 billion or 2.0 percent to $18.9 billion.

By stage of fabrication, July materials and supplies decreased 1.8 percent in durable goods and increased 0.7 percent in nondurable goods. Work in process decreased 0.1 percent in durable goods and 0.8 percent in nondurable goods. Finished goods decreased 1.1 percent in durable goods and 1.0 percent in nondurable goods.

Productivity and costs - 8:30am

Full report here

Transmission of this material is embargoed until USDL-09-1066

8:30 a.m. (EDT) Wednesday, September 2, 2009

Technical information: (202) 691-5606 • dprweb@bls.gov • www.bls.gov/lpc

Media contact: (202) 691-5902 • PressOffice@bls.gov

PRODUCTIVITY AND COSTS

Second Quarter 2009, Revised

Nonfarm business sector labor productivity increased at a 6.6 percent

annual rate during the second quarter of 2009, the U.S. Bureau of Labor

Statistics reported today. This was the largest productivity increase

since the third quarter of 2003, and reflects declines of 1.5 percent in

output and 7.6 percent in hours worked. (All quarterly percent changes in

this release are seasonally adjusted annual rates.) From the second

quarter of 2008 to the second quarter of 2009, output fell 5.5 percent

while hours fell 7.2 percent, yielding an increase in productivity of 1.9

percent (tables A and 2). Nonfarm business productivity increased at an

annual rate of 2.5 percent from 2000 through 2008.

Labor productivity, or output per hour, is calculated by dividing an index

of real output by an index of hours of all persons, including employees,

proprietors, and unpaid family workers.

Unit labor costs in nonfarm businesses fell 5.9 percent in the second

quarter of 2009, with the decline due entirely to the increase in

productivity; hourly compensation increased slightly. Unit labor costs

declined 1.2 percent over the last four quarters, as a 1.9 percent

increase in output per hour was partially offset by a 0.7 percent increase

in hourly compensation (tables A and 2).

BLS defines unit labor costs as the ratio of hourly compensation to labor

productivity; increases in hourly compensation tend to increase unit labor

costs and increases in output per hour tend to reduce them.

Productivity increased 6.5 percent in the business sector in the second

quarter of 2009. Unit labor costs decreased 6.0 percent during the second

quarter of 2009 (tables A and 1).

Manufacturing sector productivity grew 4.9 percent in the second quarter

of 2009, as output fell 9.8 percent and hours worked decreased 14.0

percent; declines in output and hours were much larger in durable goods

industries than in nondurable goods industries (tables A, 3, 4 and 5).

The productivity gain in the manufacturing sector was the largest since

the first quarter of 2005. Unit labor costs in manufacturing edged up 0.2

percent in the second quarter of 2009 and increased 6.7 percent over the

last four quarters (tables A and 3).

The data sources and methods used in the preparation of the manufacturing

output series differ from those used in preparing the business and nonfarm

business output series, and these measures are not directly comparable.

See Technical Notes for further information on data sources.

Revised measures

Table B presents previous and revised productivity and related measures

for the major sectors: business, nonfarm business and manufacturing, for

the first and second quarters of 2009.

In the second quarter of 2009, nonfarm business productivity was revised

up by 0.2 percentage point from the estimate published on August 11,

reflecting a 0.2 percentage point upward revision to output; hours were

not revised. Unit labor costs were revised down by 0.1 percentage point

in the second quarter. In the manufacturing sector, productivity was

revised down by 0.4 percentage point in the second quarter.

In the first quarter of 2009, nonfarm business productivity was not

revised. Unit labor costs fell 5.0 percent rather than decreasing 2.7

percent as previously reported, due to a 2.3 percent downward revision to

hourly compensation. In the manufacturing sector, first quarter

productivity was unrevised. Unit labor costs were revised down by 2.6

percentage points.

From the first quarter of 1987, unit labor costs, hourly compensation, and

real hourly compensation were revised in the manufacturing sector and its

subsectors. This was the result of addressing a series break between 2000

and 2001 in the manufacturing compensation series published on August 11.

The SIC-based data prior to 2001 have been linked to the NAICS-based

series. This revision eliminates the break in series at 2001 for the

manufacturing sector data based on compensation; percent changes in 2001

were revised substantially. There were small revisions to percent changes

in other years and quarters. Because the base year for the indexes (1992)

was adjusted, index values for the entire series were subject to revision.

Revised quarterly and annual series for recent years appear in tables 3-5

and revised annual indexes are displayed in appendix tables 1-3. Full

historical annual and quarterly measures can be found on the productivity

and costs home page https://www.bls.gov/lpc/#data.

More at link with formatted tables

More at link with formatted tables

ADP Employment report - 8:15am

Full report here

ADP NATIONAL EMPLOYMENT REPORT SHOWS U.S.

EMPLOYMENT DECREASED BY 298,000 PRIVATE SECTOR JOBS IN AUGUST

ROSELAND, N.J. – September 2, 2009 – According to today’s ADP National Employment Report®, private sector employment decreased by 298,000 in August. The ADP National Employment Report, created by ADP® Employer Services, a division of Automatic Data Processing, Inc. (ADP), in partnership with Macroeconomic Advisers, LLC, is derived from actual payroll data and measures the change in total nonfarm private employment each month.

Nonfarm Private Employment Highlights – August Report:

• Total employment: -298,000

• Small businesses* -122,000

• Medium businesses** -116,000

• Large businesses*** -60,000

• Goods-producing sector: -152,000

• Service-providing sector: -146,000

Addendum:

• Manufacturing industry: -74,000

* Small businesses represent payrolls with 1-49 employees

** Medium businesses represent payrolls with 50-499 employees

*** Large businesses represent payrolls with more than 499 employees

According to Joel Prakken, Chairman of Macroeconomic Advisers, LLC, “Nonfarm private employment decreased 298,000 from July to August 2009 on a seasonally adjusted basis, according to the ADP National Employment Report. August’s employment decline was the smallest since September of 2008. Employment losses are clearly diminishing. Despite recent indications that overall economic activity is stabilizing, employment, which usually trails overall economic activity, is still likely to decline for at least several more months, albeit at a diminishing rate.”

Prakken added, “August’s ADP Report estimates nonfarm private employment in the service-providing sector fell by 146,000. Employment in the goods-producing sector declined 152,000, with employment in the manufacturing sector dropping 74,000, its smallest monthly decline since July of 2008.”

“Large businesses, defined as those with 500 or more workers, saw employment decline by 60,000, while medium-size businesses with between 50 and 499 workers declined 116,000. Employment among small-size businesses, defined as those with fewer than 50 workers, declined 122,000,” said Prakken. Prakken went on to say, “In August, construction employment dropped 73,000. This was its thirty-first consecutive monthly decline, and brings the total decline in construction jobs since the peak in January 2007 to 1,562,000. Employment in the financial services sector dropped 19,000, the twenty-first consecutive monthly decline.”

More at link with formatted tables

More at link with formatted tables

Pre-market - September 2, 2009

Futures flat today waiting on economic data:

DJIA INDEX 9,303.00 0.00

S&P 500 996.40 -0.10

NASDAQ 100 1,592.25 -3.25

Today's economic calendar:

MBA Purchase Applications 7:00 AM ET

Challenger Job-Cut Report 7:30 AM ET

ADP Employment Report 8:15 AM ET

Productivity and Costs 8:30 AM ET

Factory Orders 10:00 AM ET

EIA Petroleum Status Report 10:30 AM ET

FOMC Minutes 2:00 PM ET

Today's earnings reports:

Before market opens

BF-B Brown-Forman Corporation Consumer Goods Beverages

BRLI Bio-Reference Laboratories Inc. Healthcare Medical Laboratories

BTH Blyth, Inc. Consumer Goods Personal Products

DHT DHT Maritime, Inc. Services Shipping

JOYG Joy Global, Inc. Industrial Goods Farm & Construction Machinery

SYNO Synovis Life Technologies Inc. Healthcare Medical Appliances

ZLC Zale Corporation Services Jewelry Stores

After market close:

ABM ABM Industries Inc. Services Business Services

CWST Casella Waste Systems Inc. Industrial Goods Waste Management

GEF Greif Inc. Consumer Goods Packaging & Containers

HOV Hovnanian Enterprises Inc. Industrial Goods Residential Construction

MATK Martek Biosciences Corp. Healthcare Biotechnology

NX Quanex Building Products Corporation Industrial Goods General Building Materials

OXM Oxford Industries Inc. Consumer Goods Textile - Apparel Clothing

PSS Collective Brands, Inc. Services Apparel Stores

SAI SAIC, Inc. Services Technical Services

Tuesday, September 1, 2009

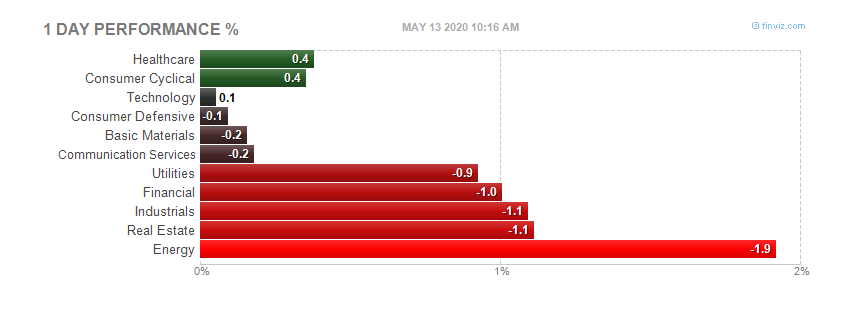

Market wrap - 5:30pm

Sell off today. The questions is - a day - or more?

Dow 9,310.60 -185.68 (-1.96%)

S&P 500 998.04 -22.58 (-2.21%)

Nasdaq 1,968.89 -40.17 (-2.00%)

Gold 957 +3 +0.32%

Oil 68.35 -1.91 -2.72%

Today by sector:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

ISM manufacturing data - 10:00am

Full report here

August 2009 Manufacturing ISM Report On Business®

PMI at 52.9%

DO NOT CONFUSE THIS NATIONAL REPORT with the various regional purchasing reports released across the country. The national report's information reflects the entire United States, while the regional reports contain primarily regional data from their local vicinities. Also, the information in the regional reports is not used in calculating the results of the national report. The information compiled in this report is for the month of August 2009.

New Orders and Production Growing

Employment and Inventories Contracting

Supplier Deliveries Slower

(Tempe, Arizona) — Economic activity in the manufacturing sector expanded in August, following 18 consecutive months of contraction, and the overall economy grew for the fourth consecutive month, say the nation's supply executives in the latest Manufacturing ISM Report On Business®.

The report was issued today by Norbert J. Ore, CPSM, C.P.M., chair of the Institute for Supply Management™ Manufacturing Business Survey Committee. "The year-and-a-half decline in manufacturing output has come to an end, as 11 of 18 manufacturing industries are reporting growth when comparing August to July. While this is certainly a positive occurrence, we have to keep in mind that it is the beginning of a new cycle and that all industries are not yet participating in the growth. The August index of 52.9 percent is the highest since June 2007. The 4 percentage point increase was driven by significant strength in the New Orders Index, which is up 9.6 points to 64.9 percent, the highest since December 2004. The growth appears sustainable in the short term, as inventories have been reduced for 40 consecutive months and supply chains will have to re-stock to meet this new demand."

PERFORMANCE BY INDUSTRY

Eleven of the 18 manufacturing industries reported growth in August. These industries — listed in order — are: Textile Mills; Apparel, Leather & Allied Products; Paper Products; Miscellaneous Manufacturing; Printing & Related Support Activities; Computer & Electronic Products; Transportation Equipment; Nonmetallic Mineral Products; Electrical Equipment, Appliances & Components; Fabricated Metal Products; and Chemical Products. The six industries reporting contraction in August — listed in order — are: Primary Metals; Plastics & Rubber Products; Furniture & Related Products; Wood Products; Food, Beverage & Tobacco Products; and Machinery.

WHAT RESPONDENTS ARE SAYING ...

* "Production is picking up as demand [for] orders is being accelerated." (Nonmetallic Mineral Products)

* "Demand from automotive manufacturers increasing thanks to 'Cash for Clunkers.'" (Fabricated Metal Products)

* "In addition to improved business come the complications of a supply chain drained of inventory." (Paper Products)

* "The sudden increase in customer demand, plus the low inventories held at services centers, is causing a shortage in the supply of raw steel." (Transportation Equipment)

* "[It] appears customers' inventories are getting low, and they are cautiously placing orders." (Apparel, Leather & Allied Products)

More at link with formatted tables

More at link with formatted tables

Construction spending - 10:00am

Full report here

JULY 2009 CONSTRUCTION AT $958.0 BILLION ANNUAL RATE

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during July 2009 was estimated at a seasonally adjusted annual rate of $958.0 billion, 0.2 percent (±1.6%)* below the revised June estimate of $959.5 billion. The July figure is 10.5 percent (±1.8%) below the July 2008 estimate of $1,070.2 billion. During the first 7 months of this year, construction spending amounted to $543.8 billion, 11.4 percent (±1.3%) below the $613.5 billion for the same period in 2008.

PRIVATE CONSTRUCTION

Spending on private construction was at a seasonally adjusted annual rate of $630.4 billion, 0.1 percent (±1.0%)* above the revised June estimate of $629.6 billion. Residential construction was at a seasonally adjusted annual rate of $245.6 billion in July, 2.3 percent (±1.3%) above the revised June estimate of $240.1 billion. Nonresidential construction was at a seasonally adjusted annual rate of $384.9 billion in July, 1.2 percent (±1.0%) below the revised June estimate of $389.5

billion.

PUBLIC CONSTRUCTION

In July, the estimated seasonally adjusted annual rate of public construction spending was $327.6 billion, 0.7 percent (±2.6%)* below the revised June estimate of $329.9 billion. Educational construction was at a seasonally adjusted annual rate of $90.8 billion, 1.3 percent (±3.7%)* below the revised June estimate of $92.0 illion. Highway construction was at a seasonally adjusted annual rate of $83.8 billion, 1.0 percent (±7.0%)* below the revised June estimate of $84.7 billion.

August 2009 data will be released on October 1, 2009 at 10:00 A.M. EDT.

For more detailed data and methodologies, go to our website:http://www.census.gov/constructionspending

Pending home sales index - 10:00am

Full report here

Washington, September 01, 2009

Contract activity for pending home sales has risen for six straight months, a pattern not seen in the history of the index since it began in 2001, according to the National Association of Realtors®.

The Pending Home Sales Index,1 a forward-looking indicator based on contracts signed in July, increased 3.2 percent to 97.6 from a reading of 94.6 in June, and is 12.0 percent higher than July 2008 when it was 87.1. The index is at the highest level since June 2007 when it was 100.7.

Lawrence Yun, NAR chief economist, said the housing market momentum has clearly turned for the better. “The recovery is broad-based across many parts of the country. Housing affordability has been at record highs this year with the added stimulus of a first-time buyer tax credit,” he said.

Pending Home Sales on a Record Roll

Washington, September 01, 2009

Contract activity for pending home sales has risen for six straight months, a pattern not seen in the history of the index since it began in 2001, according to the National Association of Realtors®.

The Pending Home Sales Index,1 a forward-looking indicator based on contracts signed in July, increased 3.2 percent to 97.6 from a reading of 94.6 in June, and is 12.0 percent higher than July 2008 when it was 87.1. The index is at the highest level since June 2007 when it was 100.7.

Lawrence Yun, NAR chief economist, said the housing market momentum has clearly turned for the better. “The recovery is broad-based across many parts of the country. Housing affordability has been at record highs this year with the added stimulus of a first-time buyer tax credit,” he said.

“Other buyers are taking advantage of low home values before prices turn higher. Nationally, the typical mortgage payment now takes less than 25 percent of a middle-income family’s monthly income to buy a median priced home, with payment percentages so far in 2009 being the lowest on record dating back to 1970. As long as home buyers stay within their budget, mortgage payments will be very manageable,” Yun said.

NAR estimates that about 1.8 to 2.0 million first-time buyers will take advantage of the $8,000 tax credit this year, with approximately 350,000 additional sales that would not have taken place without the credit. Buyers have little time to act because they must complete the transaction by November 30 to qualify for the credit. Unless extended, contracts signed but not completed by that date will not be eligible – it is taking approximately two months to complete home sales in the current market.

The Pending Home Sales Index in the Northeast declined 3.0 percent to 78.8 in July but is 4.7 percent higher than July 2008. In the Midwest the index slipped 2.0 percent to 88.1 but is 8.1 percent above a year ago. In the South, pending home sales activity rose 3.1 percent to an index of 103.8 in July and is 12.0 percent above July 2008. In the West the index jumped 12.1 percent to 112.5 and is 20.0 percent above a year ago.

NAR President Charles McMillan, a broker with Coldwell Banker Residential Brokerage in Dallas-Fort Worth, said Congress needs to keep the momentum going. “Even with a good recovery taking place, the market is not yet back to normal. With a gradual absorption of inventory, we are on the cusp of a general stabilization in home prices,” he said.

“To ensure that housing has a broad stimulus to the overall economy and stays on sound footing, we’re encouraging Congress to extend the tax credit into 2010, and to expand it to all buyers of primary residences. The faster we stabilize home prices, the fewer families will face foreclosure and the quicker credit can be extended to other sectors of the economy,” McMillan said.

NAR’s Housing Affordability Index2 stood at 158.5 in July, below the peak set in April but is still 36.0 percentage points higher than a year ago. The HAI is a broad measure of housing affordability using consistent values and assumptions over time, which examines the relationship between home prices, mortgage interest rates and family income.

Yun expects existing-home sales to rise through the fourth quarter. “Unless the tax credit is extended, no one should be surprised to see home sales drop in the first quarter of next year,” he said. “However, the fundamentals of the housing market and the economy are trending up, and we expect home sales to generally pick up in the second quarter of 2010. The buyer psychology may be shifting from, ‘Why buy now when I can purchase later,’ to ‘I don’t want to miss out on a recovery’.”

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1.2 million members involved in all aspects of the residential and commercial real estate industries.

Pre-market - September 1, 2009 - 8:10am

Futures down this morning waiting on various data later in the morning.

DJIA INDEX 9,439.00 -47.00

S&P 500 1,014.60 -5.10

NASDAQ 100 1,618.50 -6.50

Today's economic calendar:

Motor Vehicle Sales

ICSC-Goldman Store Sales 7:45 AM ET

Redbook 8:55 AM ET

ISM Mfg Index 10:00 AM ET

Construction Spending 10:00 AM ET

Pending Home Sales Index 10:00 AM ET

4-Week Bill Auction 1:00 PM ET

Today's earnings reports:

Before market opens

CMED China Medical Technologies Inc. Healthcare Medical Instruments & Supplies

CPY CPI Corp. Services Personal Services

CRMT America's Car-Mart Inc. Services Auto Dealerships

EDAP EDAP TMS SA Healthcare Medical Appliances & Equipment

GIGM GigaMedia Ltd. Technology Internet Software & Services

GMTN Gander Mountain Co. Services Specialty Retail, Other

RAIL FreightCar America Inc. Services Railroads

TUTR Plato Learning, Inc. Services Business Services

After market close

ADCT ADC Telecommunications Inc. Technology Communication Equipment

APSG Applied Signal Technology, Inc. Technology Communication Equipment

AVAV AeroVironment, Inc. Industrial Goods Aerospace/Defense Products & Services

DCI Donaldson Company Inc. Industrial Goods Pollution & Treatment Controls

PAY VeriFone Holdings, Inc. Consumer Goods Business Equipment

PIKE Pike Electric Corporation Industrial Goods General Contractors

SEAC SeaChange International Inc. Technology Processing Systems & Products

TTWO Take-Two Interactive Software Inc. Technology Multimedia & Graphics Software

Market wrap - the next morning - 8:05am

Slow market today. Gapped down at open and pretty much stayed there. Volume low, not much to get excited about.

Dow 9,496.28 -47.92 (-0.50%)

S&P 500 1,020.62 -8.31 (-0.81%)

Nasdaq 2,009.06 -19.71 (-0.97%)

Today by sector:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Monday, August 31, 2009

Pre-market - August 31,2009 - 7:45am

Futures down this morning after a sell off in Asia overnight

DJIA INDEX 9,482.00 -54.00 9,538.00

S&P 500 1,021.90 -5.50

NASDAQ 100 1,632.00 -10.50

Gold 959 12 1.21%

Oil 71.42 -1.32 -1.82%

Today's economic calendar:

Chicago PMI 9:45 AM ET

4-Week Bill Announcement 11:00 AM ET

3-Month Bill Auction 1:00 PM ET

6-Month Bill Auction 1:00 PM ET

Farm Prices 3:00 PM ET

Today's earnings reports:

Before open:

CMM China Mass Media Corp. Services Advertising Agencies

JAVA Sun Microsystems Inc. Technology Diversified Computer Systems

After close:

BNHNA Benihana Inc. Services Restaurants

CFI Culp Inc. Industrial Goods Textile Industrial

FMCN Focus Media Holding Ltd. Services Advertising Agencies

SINA Sina Corp. Technology Internet Software & Services

Subscribe to:

Posts (Atom)