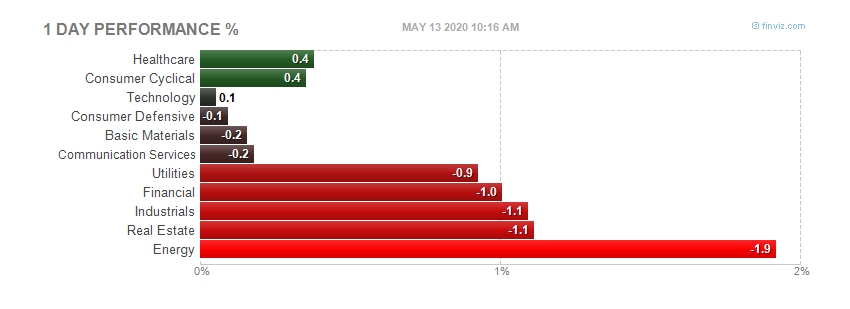

Today's heatmap:

Today's heatmap:

For the record, CNBC proclaimed today - the recession is over. Per Larry Kudlow. Larry, your still a shrill and painful to watch.

Today's heatmap:

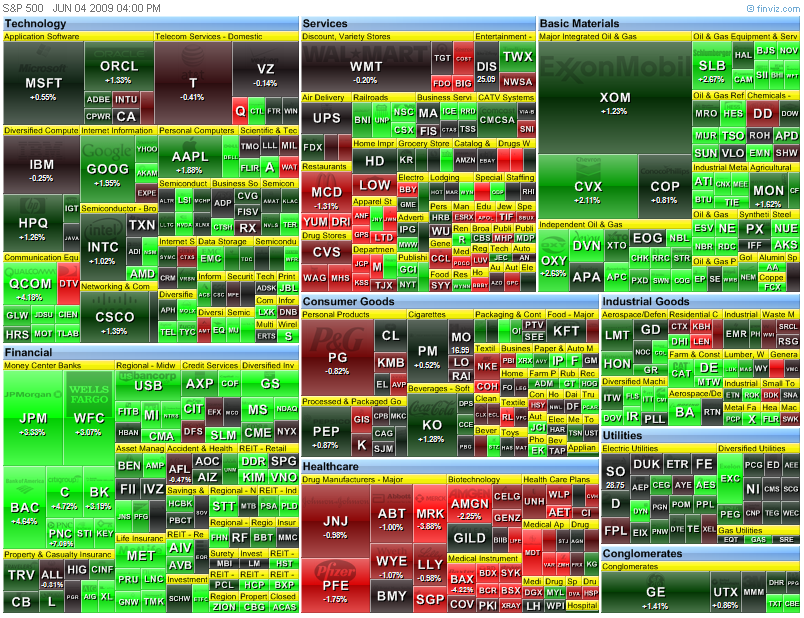

Financials! Imagine that!

Today's heatmap:

Financials! Imagine that!

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's headlines:

Goldman Sachs Raises $1.91 Billion in ICBC Stock Sale (Update1) - Bloomberg

JPMorgan, American Express Will Tap Stock Markets to Repay TARP - Boomberg

Today's headlines:

Goldman Sachs Raises $1.91 Billion in ICBC Stock Sale (Update1) - Bloomberg

JPMorgan, American Express Will Tap Stock Markets to Repay TARP - Boomberg

| Dow | 8,721.36 | +221.03 (2.60%) |

| S&P 500 | 942.87 | +23.73 (2.58%) |

| Nasdaq | 1,828.68 | +54.35 (3.06%) |

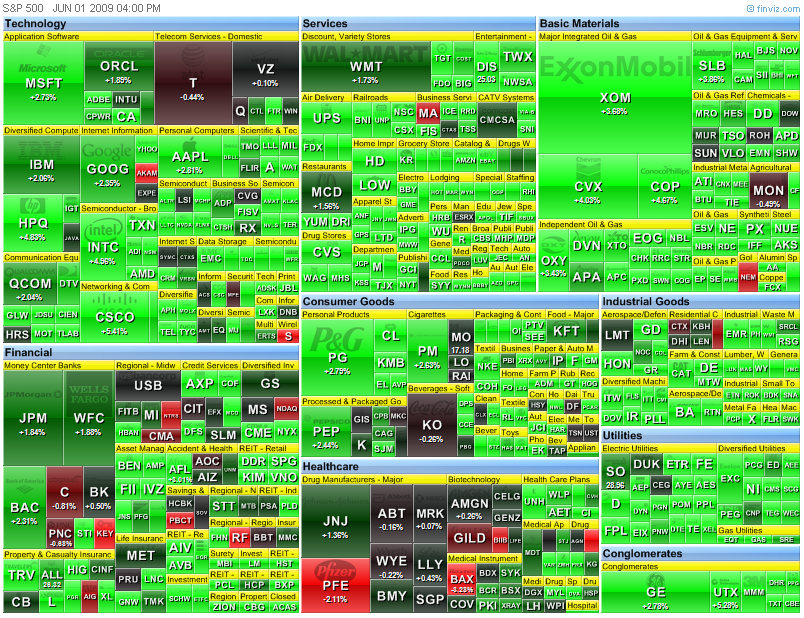

Today's heatmap:

Today's heatmap:

Looking at this chart, Friday, the SPX was around 910 2:15PM on Friday. It began to drop, going down to 905 around 2:53PM. The low was 887 Friday morning at 10:10. From 2:53 (or we can just round it to 3:00PM)it rockets to close at 919 with a huge spike in the last 5 minutes.

Today, Monday, the SPX gaps up to open significantly higher at 923. The market proceed to charge higher (on the GM news as one thing) to 942 by 10:20AM. Let's do a little math here. From 905 to 942 is 37 points. The climb took all of 2 hours between Friday afternoon and 10:20 this morning.

A couple of observations. 1)The economic data that came out last week was not all that good, and even bad in some cases. 2)The ISM and spending data that came out today was not awful, but not that good either. 3)GM, once the largest company in the world, has filed for bankruptcy. 4)We knew this was coming, probably on Monday, and considering the climb in the SPX last week, it would make a good case to be short for the weekend, no?

Looking at the huge spike in the last 5 minutes Friday, did someone NOT want to be short for Monday open? Did someone know something we, the average investor did not? Seems awful funny to me, or is this just plain Sillyness?

Anyone wonder why we call this site Sillymeter?

Looking at this chart, Friday, the SPX was around 910 2:15PM on Friday. It began to drop, going down to 905 around 2:53PM. The low was 887 Friday morning at 10:10. From 2:53 (or we can just round it to 3:00PM)it rockets to close at 919 with a huge spike in the last 5 minutes.

Today, Monday, the SPX gaps up to open significantly higher at 923. The market proceed to charge higher (on the GM news as one thing) to 942 by 10:20AM. Let's do a little math here. From 905 to 942 is 37 points. The climb took all of 2 hours between Friday afternoon and 10:20 this morning.

A couple of observations. 1)The economic data that came out last week was not all that good, and even bad in some cases. 2)The ISM and spending data that came out today was not awful, but not that good either. 3)GM, once the largest company in the world, has filed for bankruptcy. 4)We knew this was coming, probably on Monday, and considering the climb in the SPX last week, it would make a good case to be short for the weekend, no?

Looking at the huge spike in the last 5 minutes Friday, did someone NOT want to be short for Monday open? Did someone know something we, the average investor did not? Seems awful funny to me, or is this just plain Sillyness?

Anyone wonder why we call this site Sillymeter?

In case you were living in a cave, General Motors (GM) filed for bankruptcy today. And their stock is going up - it is worth NOTHING. Yep, day traders, but still.

In case you were living in a cave, General Motors (GM) filed for bankruptcy today. And their stock is going up - it is worth NOTHING. Yep, day traders, but still.