Friday, October 2, 2009

Op Ed piece from Meredith Whitney - 11:00

Link to WSJ article

The Credit Crunch Continues

Taxpayer dollars have supported institutions that are 'too big to fail.' Small business has been left out in the cold.

By MEREDITH WHITNEY

Anyone counting on a meaningful economic recovery will be greatly disappointed. How do I know? I follow credit, and credit is contracting. Access to credit is being denied at an accelerating pace. Large, well-capitalized companies have no problem finding credit. Small businesses, on the other hand, have never had a harder time getting a loan.

Since the onset of the credit crisis over two years ago, available credit to small businesses and consumers has contracted by trillions of dollars, and that phenomenon is reflected in dismal consumer spending trends. Equally worrisome are the trends in small-business credit, which has contracted at one of the fastest paces of any lending category. Small business loans are hard to find, and credit-card lines (a critical funding source to small businesses) have been cut by 25% since last year.

Unfortunately for small businesses, credit-line cuts are only about half way through. Home equity loans, also historically a key funding source for start-up small businesses, are not a source of liquidity anymore because more than 32% of U.S. homes are worth less than their mortgages.

Why do small businesses matter so much? In the U.S., small businesses employ 50% of the country's workforce and contribute 38% of GDP. Without access to credit, small businesses can't grow, can't hire, and too often end up going out of business. What's more, small businesses are often the primary source of this country's innovation. Apple, Dell, McDonald's, Starbucks were all started as small businesses.

What's especially disturbing is how taxpayer dollars have supported "too big to fail" businesses yet left small businesses unassisted and at a significant disadvantage. Small businesses do not have the same access to government guarantees on their debt. After all, most of these small businesses don't issue public debt.

As is true in most recessions, banks' commercial lending portfolios shrink as creditworthy customers pay down their debts and the less-worthy borrowers are simply denied loans. Banks, in other words, want to lend only to those that don't want to borrow. Challenging as that may be, in the last cycle small businesses at least had access to their credit cards.

Small businesses primarily fund themselves through credit cards and loans from local lenders. In the past two years, credit-card lines have been cut by over $1.25 trillion. During the same time, 10% of all credit-card accounts have been cancelled. According to the most recent Federal Reserve data, small business lending is down 3%, or $113 billion, from fourth-quarter 2008 peak levels—the first contraction since 1993. Credit cards are the most common source of liquidity to small businesses, used by 82% as a vital portion of their overall funding. Thus, it is of merit when 79% of small businesses surveyed tell the Small Business Association that credit-card lending standards have tightened drastically and their access to credit lines has decreased materially.

Incentives should be provided to smaller banks to step up small-business loans on a greater scale. Smaller banks could not only bridge gaps created by the shut down in the securitization market but also gaps being created by a massive contraction in credit-card lines. Arguably credit would perform better with these types of loans as they would reintroduce and reinforce the most important rule in banking: "Know Your Customer."

I believe that we are only in the early stages of the second half of this credit cycle. I expect another $1.5 trillion of credit-card lines to be removed from the system by the end of 2010. This includes not only the large lenders reducing exposure but also the shuttering of several major subprime credit-card lenders. Beginning in the fourth quarter of 2007, lenders began reducing available credit by zip code. During the past four quarters, lenders have cut "inactive" accounts (whether or not the customer viewed the account as a liquidity vehicle).

The next phase will likely be credit-line cuts as lenders race to pre-emptively protect themselves from regulatory changes associated with the Credit Card Accountability, Responsibility and Disclosure Act, passed in May of this year, and the 2008 Unfair and Deceptive Acts and Practices Act.

Regulators should be mindful that regulatory change during the midst of a credit crisis often ends with unintended consequences. Those same consumers that regulators are trying to help are actually being hurt by a vast reduction in available credit.

Main Street represents the foundation of this country. Reviving it should take priority over any regulatory reform or systemic overhaul.

Ms. Whitney is CEO of Meredith Whitney Advisory Group, LLC.

Factory orders - 10:00am

Full report here

August 2009 --------------- Released 10:00 A.M. EDT October 2, 2009

(M3-2(09)-08)

Note: All figures in text are in seasonally adjusted current dollars

For Data - (301) 763-4673

For Questions - Chris Savage or Jessica Young

(301) 763-4832

Summary

New orders for manufactured goods in August, down following four consecutive monthly increases, decreased $2.8 billion or 0.8 percent to $352.9 billion, the U.S. Census Bureau reported today. This followed a 1.4 percent July increase. Excluding transportation, new orders increased 0.4 percent. Shipments, down following two consecutive monthly increases, decreased $0.9 billion or 0.3 percent to $360.0 billion. This followed a 0.3 percent July increase. Unfilled orders, down eleven consecutive months, decreased $3.1 billion or 0.4 percent to $736.8 billion. This was the longest streak of consecutive monthly decreases since the series was first published on a NAICS basis in 1992. This followed a 0.1 percent July decrease. The unfilled orders-to-shipments ratio was 5.98, up from 5.94 in July. Inventories, down twelve consecutive months, decreased $3.9 billion or 0.8 percent to $498.2 billion. This was the longest streak of consecutive monthly decreases since February 2001-May 2002 and followed a 0.9 percent July decrease. The inventories-to-shipments ratio was 1.38, down from 1.39 in July.

New Orders

New orders for manufactured durable goods in August, down two of the last three months, decreased $4.4 billion or 2.6 percent to $164.1 billion, revised from the previously published 2.4 percent decrease. This followed a 4.8 percent July increase.

New orders for manufactured nondurable goods increased $1.5 billion or 0.8 percent to $188.7 billion.

Shipments

Shipments of manufactured durable goods in August, down following two consecutive monthly increases, decreased $2.4 billion or 1.4 percent to $171.3 billion, unchanged from the previously published decrease. This followed a 2.3 percent July increase.

Shipments of manufactured nondurable goods, up three of the last four months, increased $1.5 billion or 0.8 percent to $188.7 billion. This followed a 1.5 percent July decrease. This increase was due to petroleum and coal products, which increased $1.9 billion or 5.4 percent to $36.7 billion.

Unfilled Orders

Unfilled orders for manufactured durable goods in August, down eleven consecutive months, decreased $3.1 billion or 0.4 percent to $736.8 billion, unchanged from the previously published decrease. This was the longest streak of consecutive monthly decreases since the series was first published on a NAICS basis in 1992 and followed a 0.1 percent July decrease.

Inventories

Inventories of manufactured durable goods in August, down eight consecutive months, decreased $4.5 billion or 1.4 percent to $308.4 billion, revised from the previously published 1.3 percent decrease. This followed a 1.2 percent July decrease.

Inventories of manufactured nondurable goods, up following eleven consecutive monthly decreases, increased $0.6 billion or 0.3 percent to $189.9 billion. This followed a 0.4 percent July decrease. Petroleum and coal products drove the increase, up $0.7 billion or 2.8 percent to $27.4 billion.

By stage of fabrication, August materials and supplies decreased 0.8 percent in durable goods and 0.1 percent in nondurable goods. Work in process decreased 2.3 percent in durable goods and increased 1.4 percent in nondurable goods. Finished goods decreased 1.0 percent in durable goods and increased 0.1 percent in nondurable goods.

Employment report - 8:30am

Opps!

Full report here

THE EMPLOYMENT SITUATION -- SEPTEMBER 2009

Nonfarm payroll employment continued to decline in September (-263,000), and

the unemployment rate (9.8 percent) continued to trend up, the U.S. Bureau of

Labor Statistics reported today. The largest job losses were in construction,

manufacturing, retail trade, and government.

Household Survey Data

Since the start of the recession in December 2007, the number of unemployed

persons has increased by 7.6 million to 15.1 million, and the unemployment

rate has doubled to 9.8 percent. (See table A-1.)

Unemployment rates for the major worker groups--adult men (10.3 percent),

adult women (7.8 percent), teenagers (25.9 percent), whites (9.0 percent),

blacks (15.4 percent), and Hispanics (12.7 percent)--showed little change

in September. The unemployment rate for Asians was 7.4 percent, not season-

ally adjusted. The rates for all major worker groups are much higher than

at the start of the recession. (See tables A-1, A-2, and A-3.)

Among the unemployed, the number of job losers and persons who completed

temporary jobs rose by 603,000 to 10.4 million in September. The number of

long-term unemployed (those jobless for 27 weeks and over) rose by 450,000

to 5.4 million. In September, 35.6 percent of unemployed persons were job-

less for 27 weeks or more. (See tables A-8 and A-9.)

The civilian labor force participation rate declined by 0.3 percentage point

in September to 65.2 percent. The employment-population ratio, at 58.8 per-

cent, also declined over the month and has decreased by 3.9 percentage points

since the recession began in December 2007. (See table A-1.)

In September, the number of persons working part time for economic reasons

(sometimes referred to as involuntary part-time workers) was little changed

at 9.2 million. The number of such workers rose sharply throughout most of

the fall and winter but has been little changed since March. (See table A-5.)

About 2.2 million persons were marginally attached to the labor force in

September, an increase of 615,000 from a year earlier. (The data are not sea-

sonally adjusted.) These individuals were not in the labor force, wanted and

were available for work, and had looked for a job sometime in the prior 12

months. They were not counted as unemployed because they had not searched for

work in the 4 weeks preceding the survey. (See table A-13.)

Among the marginally attached, there were 706,000 discouraged workers in

September, up by 239,000 from a year earlier. (The data are not seasonally

adjusted.) Discouraged workers are persons not currently looking for work

because they believe no jobs are available for them. The other 1.5 million

persons marginally attached to the labor force in September had not searched

for work in the 4 weeks preceding the survey for reasons such as school

attendance or family responsibilities.

Establishment Survey Data

Total nonfarm payroll employment declined by 263,000 in September. From May

through September, job losses averaged 307,000 per month, compared with los-

ses averaging 645,000 per month from November 2008 to April. Since the start

of the recession in December 2007, payroll employment has fallen by 7.2 mil-

lion. (See table B-1.)

In September, construction employment declined by 64,000. Monthly job los-

ses averaged 66,000 from May through September, compared with an average of

117,000 per month from November to April. September job cuts were concen-

trated in the industry's nonresidential components (-39,000) and in heavy

construction (-12,000). Since December 2007, employment in construction has

fallen by 1.5 million.

Employment in manufacturing fell by 51,000 in September. Over the past 3

months, job losses have averaged 53,000 per month, compared with an average

monthly loss of 161,000 from October to June. Employment in manufacturing

has contracted by 2.1 million since the onset of the recession.

In the service-providing sector, the number of jobs in retail trade fell by

39,000 in September. From April through September, retail employment has

fallen by an average of 29,000 per month, compared with an average monthly

loss of 68,000 for the prior 6-month period.

Government employment was down by 53,000 in September, with the largest

decline occurring in the non-education component of local government

(-24,000).

Employment in health care continued to increase in September (19,000), with

the largest gain occurring in ambulatory health care services (15,000).

Health care has added 559,000 jobs since the beginning of the recession,

although the average monthly job gain thus far in 2009 (22,000) is down from

the average monthly gain during 2008 (30,000).

Employment in transportation and warehousing continued to trend down in

September. The number of jobs in financial activities, professional and

business services, leisure and hospitality, and information showed little

or no change over the month.

In September, the average workweek for production and nonsupervisory workers

on private nonfarm payrolls edged down by 0.1 hour to 33.0 hours. Both the

manufacturing workweek and factory overtime decreased by 0.1 hour over the

month, to 39.8 and 2.8 hours, respectively. (See table B-2.)

In September, average hourly earnings of production and nonsupervisory

workers on private nonfarm payrolls edged up by 1 cent, or 0.1 percent, to

$18.67. Over the past 12 months, average hourly earnings have risen by 2.5

percent, while average weekly earnings have risen by only 0.7 percent due

to declines in the average workweek. (See table B-3.)

The change in total nonfarm payroll employment for July was revised from

-276,000 to -304,000, and the change for August was revised from -216,000

to -201,000.

More at link with formatted tables

Pre-market - Friday, October 2, 2009

Futures down this morning waiting on the jobs report at 8:30

DJIA INDEX 9,439.00 -32.00

S&P 500 1,024.50 -2.90

NASDAQ 100 1,665.50 -5.00

Today's economic calendar:

Employment Situation 8:30 AM ET

Factory Orders 10:00 AM ET

Today's earnings reports:

NONE

Thursday, October 1, 2009

Market wrap - 4:30

Wow! Do I see Bears eating green shoots? They did today.

Dow 9,509 -203 -2.09%

Nasdaq 2,057 -65 -3.06%

S&P 500 1,030 -27 -2.58%

GlobalDow 1,855 -40 -2.09%

Gold 1,001 -9 -0.85%

Oil 70.32 0.21 0.30%

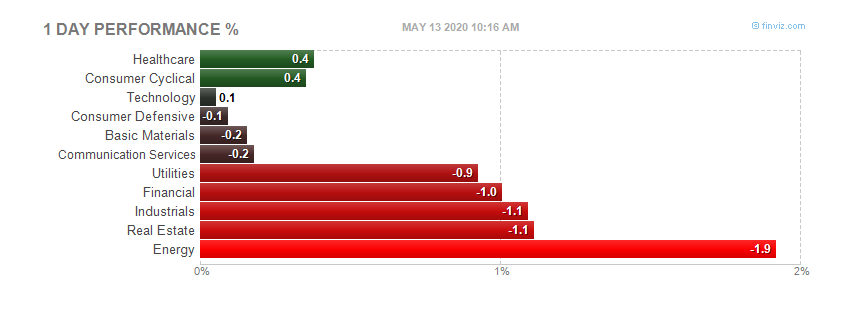

Today by sector:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

New home sales index report - 10:00am

Full report here

Washington, October 01, 2009

Pending home sales have increased for seven straight months, the longest in the series of the index which began in 2001, according to the National Association of Realtors®.

The Pending Home Sales Index,* a forward-looking indicator based on contracts signed in August, rose 6.4 percent to 103.8 from a reading of 97.6 in July, and is 12.4 percent above August 2008 when it was 92.4. The index is at the highest level since March 2007 when it was 104.5.

Lawrence Yun, NAR chief economist, said not all contracts are turning into closed sales within an expected timeframe. “The rise in pending home sales shows buyers are returning to the market and signing contracts, but deals are not necessarily closing because of long delays related to short sales, and issues regarding complex new appraisal rules,” he said. “No doubt many first-time buyers are rushing to beat the deadline for the $8,000 tax credit, which expires at the end of next month.”

The Pending Home Sales Index in the Northeast jumped 8.2 percent to 85.3 in August and is 12.0 percent higher than August 2008. In the Midwest the index rose 3.1 percent to 90.8 in August and is 7.6 percent above a year ago. In the South, pending home sales increased 0.8 percent to an index of 104.6 and is 8.2 percent above August 2008. In the West the index surged 16.0 percent to 130.5 and is 22.3 percent above a year ago.

“There is likely to be some double counting over a span of several months because some buyers whose contracts were cancelled have found another home and signed a new contract to buy,” Yun explained. “Perhaps the real question is how many transactions are being delayed in the pipeline, and how many are being cancelled? Without historic precedents, it’s challenging to assess.”

Yun also noted that the data sample coverage for pending sales is smaller than the measurement for closed existing-home sales, so the two series will never match one for one.

NAR President Charles McMillan, a broker with Coldwell Banker Residential Brokerage in Dallas-Fort Worth, said first-time buyers need to act now. “Potential first-time buyers must make a contract offer very soon to have a reasonable chance of qualifying for the tax credit,” he said. “Congress needs to extend and expand this program because it’s stimulating the economy and reducing inventory close to price stabilization points.”

McMillan said a sizable number of homebuyers already in the pipeline could be let down because of the tight deadline. “We know there is a pent-up demand because sales are below normal levels for the size of our population. The faster we absorb excess inventory, the sooner we’ll turn the corner on home prices, prevent additional families from becoming upside-down in their mortgages, and give Wall Street the confidence to extend credit to other sectors,” he said. “Each home sale pumps an additional $63,000 into the economy through related goods and services, so the benefits of extending and expanding the tax credit far outweigh the costs.”

Yun said the forecast for home sales and prices depends very much on whether a tax credit is extended. “All we can say for certain is sales will decline when the tax credit expires because we are not yet on a self-sustaining recovery path. It also raises a risk of a double-dip recession,” he said. “Extending and expanding the tax credit is the best tool in our arsenal to encourage financially qualified buyers to stimulate the economy and help reduce the budget deficit.”

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1.2 million members involved in all aspects of the residential and commercial real estate industries.

Construction spending - 10:00am

Full report here

AUGUST 2009 CONSTRUCTION AT $941.9 BILLION ANNUAL RATE

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during August 2009 was estimated at a seasonally adjusted annual rate of $941.9 billion, 0.8 percent (±1.8%)* above the revised July

estimate of $934.6 billion. The August figure is 11.6 percent (±1.8%) below the August 2008 estimate of $1,066.1 billion. During the first 8 months of this year, construction spending amounted to $629.5 billion, 11.9 percent (±1.3%) below the $714.3 billion for the same period in 2008.

PRIVATE CONSTRUCTION

Spending on private construction was at a seasonally adjusted annual rate of $622.1 billion, 1.8 percent (±1.1%) above the revised July estimate of $611.1 billion. Residential construction was at a seasonally adjusted annual rate of $249.5 billion

in August, 4.7 percent (±1.3%) above the revised July estimate of $238.3 billion. Nonresidential construction was at a seasonally adjusted annual rate of $372.6 billion in August, 0.1 percent (±1.1%)* below the revised July estimate of $372.8 billion.

PUBLIC CONSTRUCTION

In August, the estimated seasonally adjusted annual rate of public construction spending was $319.8 billion, 1.1 percent (±2.7%)* below the revised July estimate of $323.5 billion. Educational construction was at a seasonally adjusted annual

rate of $89.2 billion, nearly the same as (±4.2%)* the revised July estimate of $89.3 billion. Highway construction was at a seasonally adjusted annual rate of $85.2 billion, 0.8 percent (±7.5%)* above the revised July estimate of $84.5 billion.

More at link.

ISM report - 10:00am

Full report here

September 2009 Manufacturing ISM Report On Business®

PMI at 52.6%

DO NOT CONFUSE THIS NATIONAL REPORT with the various regional purchasing reports released across the country. The national report's information reflects the entire United States, while the regional reports contain primarily regional data from their local vicinities. Also, the information in the regional reports is not used in calculating the results of the national report. The information compiled in this report is for the month of September 2009.

New Orders and Production Growing

Employment and Inventories Contracting

Supplier Deliveries Slower

(Tempe, Arizona) — Economic activity in the manufacturing sector expanded in September for the second consecutive month, and the overall economy grew for the fifth consecutive month, say the nation's supply executives in the latest Manufacturing ISM Report On Business®.

The report was issued today by Norbert J. Ore, CPSM, C.P.M., chair of the Institute for Supply Management™ Manufacturing Business Survey Committee. "The manufacturing sector grew for the second consecutive month in September. While the rate of growth moderated slightly when compared to August, the recovery broadened as the number of industries reporting growth increased from 11 to 13. Both new orders and production are growing, but at a slower rate when compared to August. It appears the fundamentals for continuing recovery are still at work as inventories and sales are gaining balance. This month, we asked a special question with regard to the American Recovery and Reinvestment Act. Twelve of the 18 manufacturing industries expect to derive some benefit from the program, and 12 manufacturing industries responded that they expect their companies to see some benefit."

PERFORMANCE BY INDUSTRY

In September, 13 of the 18 manufacturing industries reported growth. The industries — listed in order — are: Wood Products; Paper Products; Apparel, Leather & Allied Products; Transportation Equipment; Textile Mills; Printing & Related Support Activities; Petroleum & Coal Products; Electrical Equipment, Appliances & Components; Fabricated Metal Products; Chemical Products; Computer & Electronic Products; Miscellaneous Manufacturing; and Food, Beverage & Tobacco Products. The four industries reporting contraction in September are: Primary Metals; Furniture & Related Products; Plastics & Rubber Products; and Machinery.

WHAT RESPONDENTS ARE SAYING ...

* "Purchasing remains a challenge as suppliers now seem to be trying to raise pricing at any sign of life in the economy." (Computer & Electronic Products)

* "Business is picking up — lots of opportunities." (Primary Metals)

* "Agricultural commodities continue to weaken, with the exception of the domestic and world sugar markets." (Food, Beverage & Tobacco Products)

* "Automotive demand continues to be strong even after 'cash for clunkers.'" (Fabricated Metal Products)

* "Business remains slow, with no sign of improvement again this month." (Nonmetallic Mineral Products)

More at link

Jobless claims - 8:30am

Opps! But good news, not as bad as expected. CNBC giddy over the numbers.

Full report here

UNEMPLOYMENT INSURANCE WEEKLY CLAIMS REPORT

SEASONALLY ADJUSTED DATA

In the week ending Sept. 26, the advance figure for seasonally adjusted initial claims was 551,000, an increase of 17,000 from the previous week's revised figure of 534,000. The 4-week moving average was 548,000, a decrease of 6,250 from the previous week's revised average of 554,250.

The advance seasonally adjusted insured unemployment rate was 4.6 percent for the week ending Sept. 19, unchanged from the prior week's unrevised rate of 4.6 percent.

The advance number for seasonally adjusted insured unemployment during the week ending Sept. 19 was 6,090,000, a decrease of 70,000 from the preceding week's revised level of 6,160,000. The 4-week moving average was 6,154,500, a decrease of 39,250 from the preceding week's revised average of 6,193,750.

The fiscal year-to-date average for seasonally adjusted insured unemployment for all programs is 5.665 million.

UNADJUSTED DATA

The advance number of actual initial claims under state programs, unadjusted, totaled 443,694 in the week ending Sept. 26, an increase of 5,878 from the previous week. There were 392,515 initial claims in the comparable week in 2008.

The advance unadjusted insured unemployment rate was 3.8 percent during the week ending Sept. 19, a decrease of 0.1 percentage point from the prior week. The advance unadjusted number for persons claiming UI benefits in state programs totaled 5,054,617, a decrease of 169,287 from the preceding week. A year earlier, the rate was 2.3 percent and the volume was 3,018,976.

Extended benefits were available in Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, the District of Columbia, Florida, Georgia, Idaho, Illinois, Indiana, Kansas, Kentucky, Maine, Massachusetts, Michigan, Minnesota, Missouri, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, Oregon, Pennsylvania, Puerto Rico, Rhode Island, South Carolina, Tennessee, Texas, Vermont, Virginia, Washington, West Virginia, and Wisconsin during the week ending Sept. 12.

Initial claims for UI benefits by former Federal civilian employees totaled 1,455 in the week ending Sept. 19, an increase of 323 from the prior week. There were 2,296 initial claims by newly discharged veterans, an increase of 367 from the preceding week.

There were 20,408 former Federal civilian employees claiming UI benefits for the week ending Sept. 12, an increase of 1,202 from the previous week. Newly discharged veterans claiming benefits totaled 30,689, an increase of 457 from the prior week.

States reported 3,275,213 persons claiming EUC (Emergency Unemployment Compensation) benefits for the week ending Sept. 12, an increase of 99,832 from the prior week. There were 1,559,198 claimants in the comparable week in 2008. EUC weekly claims include both first and second tier activity.

The highest insured unemployment rates in the week ending Sept. 12 were in Puerto Rico (6.1 percent), Oregon (5.4), Nevada (5.3), Pennsylvania (5.3), California (4.9), Michigan (4.9), Wisconsin (4.8), New Jersey (4.7), North Carolina (4.7), Arkansas (4.6), and South Carolina (4.6).

The largest increases in initial claims for the week ending Sept. 19 were in California (+5,112), Texas (+3,946), Florida (+2,348), Iowa (+2,013), and Illinois (+1,945), while the largest decreases were in Kansas (-1,545), Wisconsin (-1,258), Oregon (-833), Ohio (-804), and New York (-623).

More at link with formatted tables

Futures down this morning waiting on economic data.

DJIA INDEX 9,609.00 -44.00

S&P 500 1,046.50 -6.40

NASDAQ 100 1,706.75 -10.75

Today's economic reports:

Monster Employment Index

Motor Vehicle Sales

Challenger Job-Cut Report 7:30 AM ET

Personal Income and Outlays 8:30 AM ET

Jobless Claims 8:30 AM ET

Ben Bernanke Speaks 9:00 AM ET

30-Yr Bond Announcement 9:00 AM ET

ISM Mfg Index 10:00 AM ET

Construction Spending 10:00 AM ET

Pending Home Sales Index 10:00 AM ET

EIA Natural Gas Report 10:30 AM ET

3-Month Bill Announcement 11:00 AM ET

6-Month Bill Announcement 11:00 AM ET

3-Yr Note Announcement 11:00 AM ET

10-Yr Note Announcement 11:00 AM ET

10-Yr TIPS Announcement 11:00 AM ET

Today's earnings reports:

Before open:

CRAI CRA International Inc. Services Management Services

MTRX Matrix Service Co. Industrial Goods Heavy Construction

STZ Constellation Brands Inc. Consumer Goods Beverages - Wineries & Distillers

After close:

ACN Accenture plc Services Management Services

BLUD Immucor Inc. Healthcare Diagnostic Substances

CREL Corel Corporation Technology Multimedia & Graphics Software

DMAN DemandTec, Inc. Technology Business Software & Services

GPN Global Payments Inc. Services Business Services

RECN Resources Connection Inc. Services Management Services

SMOD SMART Modular Technologies (WWH) Inc. Technology Semiconductor - Integrated Circuits

SMSC Standard Microsystems Corp. Technology Semiconductor - Integrated Circuits

TSCM TheStreet.com, Inc. Technology Internet Information Providers

Wednesday, September 30, 2009

GDP - 8:30am

Full report here

GROSS DOMESTIC PRODUCT: SECOND QUARTER 2009 (THIRD ESTIMATE)

CORPORATE PROFITS: SECOND QUARTER 2009 (REVISED ESTIMATE)

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- decreased at an annual rate of 0.7 percent in the second quarter of 2009, (that is, from the first quarter to the second quarter), according to the "third" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP decreased 6.4 percent.

The GDP estimate released today is based on more complete source data than were available for the "second" estimate issued last month. In the second estimate, the decrease in real GDP was 1.0 percent (see "Revisions" on page 3).

The decrease in real GDP in the second quarter primarily reflected negative contributions from private inventory investment, nonresidential fixed investment, residential fixed investment, personal consumption expenditures (PCE), and exports that were partly offset by positive contributions from federal government spending and state and local government spending. Imports, which are a subtraction

in the calculation of GDP, decreased.

The much smaller decrease in real GDP in the second quarter than in the first primarily reflected much smaller decreases in nonresidential fixed investment and in exports, an upturn in federal government spending, a smaller decrease in private inventory investment, an upturn in state and local government spending, and a smaller decrease in residential fixed investment that were partly offset by a

much smaller decrease in imports and a downturn in PCE.

_________________________________________________

FOOTNOTE.--Quarterly estimates are expressed at seasonally adjusted annual rates, unless otherwise specified. Quarter-to-quarter dollar changes are differences between these published estimates. Percent changes are calculated from unrounded data and are annualized. “Real” estimates are in chained (2005) dollars. Price indexes are chain-type measures.

This news release is available on BEA’s Web site along with the Technical Note and Highlights related to this release.

_________________________________________________

Motor vehicle output added 0.19 percentage point to the second-quarter change in real GDP after subtracting 1.69 percentage points from the first-quarter change. Final sales of computers subtracted 0.04 percentage point from the second-quarter change in real GDP after adding 0.06 percentage point to the first-quarter change.

The price index for gross domestic purchases, which measures prices paid by U.S. residents, increased 0.5 percent in the second quarter, the same increase as in the second estimate; this index decreased 1.4 percent in the first quarter. Excluding food and energy prices, the price index for gross domestic purchases increased 0.8 percent in the second quarter, compared with an increase of 0.2

percent in the first.

Real personal consumption expenditures decreased 0.9 percent in the second quarter, in contrast to an increase of 0.6 percent in the first. Real nonresidential fixed investment decreased 9.6 percent, compared with a decrease of 39.2 percent. Nonresidential structures decreased 17.3 percent, compared with a decrease of 43.6 percent. Equipment and software decreased 4.9 percent, compared with a decrease of 36.4 percent. Real residential fixed investment decreased 23.3 percent, compared with a decrease of 38.2 percent.

Real exports of goods and services decreased 4.1 percent in the second quarter, compared with a decrease of 29.9 percent in the first. Real imports of goods and services decreased 14.7 percent, compared with a decrease of 36.4 percent.

Real federal government consumption expenditures and gross investment increased 11.4 percent in the second quarter, in contrast to a decrease of 4.3 percent in the first. National defense increased 14.0 percent, in contrast to a decrease of 5.1 percent. Nondefense increased 6.1 percent, in contrast to a decrease of 2.5 percent. Real state and local government consumption expenditures and gross

investment increased 3.9 percent, in contrast to a decrease of 1.5 percent.

The change in real private inventories subtracted 1.42 percentage points from the second-quarter change in real GDP, after subtracting 2.36 percentage points from the first-quarter change. Private businesses decreased inventories $160.2 billion in the second quarter, following a decrease of $113.9 billion in the first quarter and a decrease of $37.4 billion in the fourth.

Real final sales of domestic product -- GDP less change in private inventories -- increased 0.7 percent in the second quarter, in contrast to a decrease of 4.1 percent in the first.

Gross domestic purchases

Real gross domestic purchases -- purchases by U.S. residents of goods and services wherever produced -- decreased 2.3 percent in the second quarter, compared with a decrease of 8.6 percent in the first.

Gross national product

Real gross national product -- the goods and services produced by the labor and property supplied by U.S. residents -- decreased 1.0 percent in the second quarter, compared with a decrease of 6.6 percent in the first. GNP includes, and GDP excludes, net receipts of income from the rest of the world, which decreased $7.4 billion in the second quarter after decreasing $6.1 billion in the first; in the

second quarter, receipts decreased $8.4 billion, and payments decreased $1.0 billion.

Current-dollar GDP

Current-dollar GDP -- the market value of the nation's output of goods and services -- decreased 0.8 percent, or $26.8 billion, in the second quarter to a level of $14,151.2 billion. In the first quarter, current-dollar GDP decreased 4.6 percent, or $169.3 billion.

Revisions

The “third” estimate of the second-quarter is 0.3 percentage point less of a decrease, or $9.0 billion higher, than the "second" estimate issued last month. The upward revision to real GDP primarily reflected an upward revision to nonresidential fixed investment.

Advance Estimate Second Estimate Third Estimate

(Percent change from preceding quarter)

Real GDP................................. -1.0 -1.0 -0.7

Current-dollar GDP....................... -0.8 -1.0 -0.8

Gross domestic purchases price index..... 0.7 0.5 0.5

Corporate Profits

Profits from current production (corporate profits with inventory valuation and capital consumption adjustments) increased $43.8 billion in the second quarter, compared with an increase of $59.1 billion in the first quarter. Current-production cash flow (net cash flow with inventory valuation adjustment) -- the internal funds available to corporations for investment -- decreased $30.5 billion in

the second quarter, in contrast to an increase of $16.2 billion in the first.

Taxes on corporate income increased $35.6 billion in the second quarter, compared with an increase of $47.0 billion in the first. Profits after tax with inventory valuation and capital consumption adjustments increased $8.2 billion in the second quarter, compared with an increase of $12.0 billion in the first. Dividends decreased $62.1 billion, compared with a decrease of $51.8 billion; current-

production undistributed profits increased $70.3 billion, compared with an increase of $63.7 billion.

Domestic profits of financial corporations increased $28.5 billion in the second quarter, compared with an increase of $115.9 billion in the first. Domestic profits of nonfinancial corporations increased $29.8 billion in the second quarter, in contrast to a decrease of $40.2 billion in the first. In the second quarter, real gross value added of nonfinancial corporations decreased, and profits per unit of real value added increased. The increase in unit profits reflected decreases in unit labor and nonlabor costs that more than offset a decrease in unit prices.

The rest-of-the-world component of profits decreased $14.6 billion in the second quarter, compared with a decrease of $16.6 billion in the first. This measure is calculated as (1) receipts by U.S. residents of earnings from their foreign affiliates plus dividends received by U.S. residents from unaffiliated foreign corporations minus (2) payments by U.S. affiliates of earnings to their foreign

parents plus dividends paid by U.S. corporations to unaffiliated foreign residents. The second-quarter decrease was accounted for by a larger increase in payments than in receipts.

Profits before tax with inventory valuation adjustment is the best available measure of industry profits because estimates of the capital consumption adjustment by industry do not exist. This measure reflects depreciation-accounting practices used for federal income tax returns. According to this measure, domestic profits of both financial and nonfinancial corporations increased. The increase in nonfinancial corporations reflected increases in retail trade, in manufacturing, and in information that were partly offset by decreases in wholesale trade and in transportation and warehousing. Within manufacturing, the largest increases were in motor vehicles, in “other” nondurable goods, and in chemical products. The largest decrease was in petroleum and coal products.

Profits before tax increased $90.6 billion in the second quarter, compared with an increase of $186.4 billion in the first. The before-tax measure of profits does not reflect, as does profits from current production, the capital consumption and inventory valuation adjustments. These adjustments convert depreciation of fixed assets and inventory withdrawals reported on a tax-return, historical-cost

basis to the current-cost measures used in the national income and product accounts. The capital consumption adjustment increased $16.3 billion in the second quarter (from -$144.9 billion to -$128.6 billion), in contrast to a decrease of $69.3 billion in the first. The inventory valuation adjustment decreased $63.0 billion (from $81.1 billion to $18.1 billion), compared with a decrease of $58.1 billion.

ADP Employment report - 8:15am

Full report here

Wednesday, September 30, 2009, 8:15 A.M. ET

Nonfarm private employment decreased 254,000 from August to September 2009 on a seasonally adjusted basis, according to the ADP National Employment Report®. The estimated change of employment from July to August was revised by 21,000, from a decline of 298,000 to a decline of 277,000.

September’s employment decline was the smallest since July of 2008 and employment losses have diminished significantly over the last two quarters. Nevertheless, employment, which usually trails overall economic activity, is likely to decline for at least several more months, with losses continuing to diminish.

September’s ADP Report estimates nonfarm private employment in the service-providing sector fell by 103,000. Employment in the goods-producing sector declined 151,000, with employment in the manufacturing sector dropping 74,000, about the same as last month.

Large businesses, defined as those with 500 or more workers, saw employment decline by 61,000, while medium-size businesses with between 50 and 499 workers declined 93,000. Employment among small-size businesses, defined as those with fewer than 50 workers, declined 100,000. Employment losses among small-size businesses have diminished in each of the last six months.

In September, construction employment dropped 73,000. This was its thirty-second consecutive monthly decline, and brings the total decline in construction jobs since the peak in January 2007 to 1,632,000. Employment in the financial services sector dropped 19,000, the twenty-second consecutive monthly decline.

Pre-market - Wednesday, September 30, 2009

Futures up slightly this morning:

DJIA INDEX 9,704.00 31.00

S&P 500 1,058.80 4.00

NASDAQ 100 1,721.75

Today's economic calendar:

MBA Purchase Applications 7:00 AM ET

ADP Employment Report 8:15 AM ET

GDP 8:30 AM ET

Corporate Profits 8:30 AM ET

Chicago PMI 9:45 AM ET

EIA Petroleum Status Report 10:30 AM ET

Today's earnings reports:

Before open: ATU

After close:

AEHR Aehr Test Systems Technology Semiconductor Equipment & Materials

DMND Diamond Foods, Inc. Consumer Goods Processed & Packaged Goods

LWSN Lawson Software, Inc. Technology Application Software

OHB Orleans Homebuilders Inc. Industrial Goods Residential Construction

XRTX Xyratex Ltd. Technology Data Storage Devices

Market wrap - Wed edition

Dow 9,742 -47 -0.48%

Nasdaq 2,124 -7 -0.31%

S&P 500 1,061 -2 -0.22%

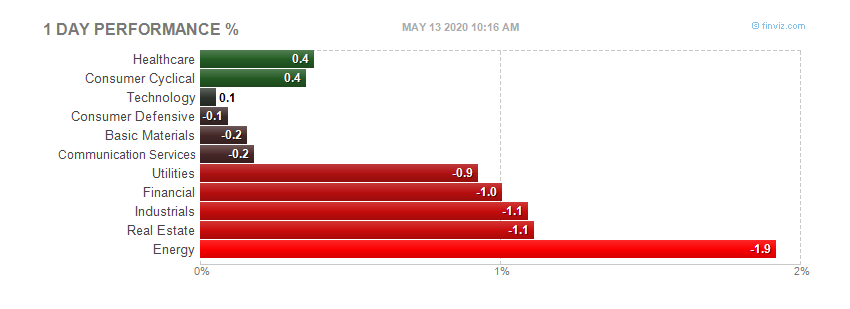

Today by sector:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Tuesday, September 29, 2009

Consumer Confidence - 10:00

Full report here

The Conference Board Consumer Confidence Index® Dips in September

September 29, 2009

The Conference Board Consumer Confidence Index®, which had improved in August, dipped in September. The Index now stands at 53.1 (1985=100), down from 54.5 in August. The Present Situation Index decreased to 22.7 from 25.4. The Expectations Index declined to 73.3 from 73.8 last month.

The Consumer Confidence Survey® is based on a representative sample of 5,000 U.S. households. The monthly survey is conducted for The Conference Board by TNS. TNS is the world's largest custom research company. The cutoff date for September's preliminary results was September 22nd.

Says Lynn Franco, Director of The Conference Board Consumer Research Center: "Consumer Confidence, which had improved in August, retreated slightly in September. The Present Situation Index decreased, as consumers viewed both current business conditions and the labor market less favorably than last month. While not as pessimistic as earlier this year, consumers remain quite apprehensive about the short-term outlook and their incomes. With the holiday season quickly approaching, this is not very encouraging news."

Consumers' assessment of current conditions was less favorable in September. Those claiming business conditions are "bad" increased to 46.3 percent from 44.6 percent, while those claiming conditions are "good" increased to 8.7 percent from 8.5 percent. Consumers' appraisal of the job market was also less favorable. Those claiming jobs are "hard to get" increased to 47.0 percent from 44.3 percent, while those claiming jobs are "plentiful" decreased to 3.4 percent from 4.3 percent.

Consumers' short-term outlook was also slightly more pessimistic. Those anticipating an improvement in business conditions over the next six months decreased to 21.3 percent from 22.2 percent, while those expecting conditions to worsen decreased to 15.0 percent from 15.2 percent.

The labor market outlook was virtually unchanged. Those expecting more jobs in the months ahead edged down to 17.9 percent from 18.0 percent, while those expecting fewer jobs remained the same at 23.1 percent. The proportion of consumers expecting an increase in their incomes increased slightly to 11.2 percent from 10.8 percent.

Case Shiller HPI - 9:00am

Full report here

Broad Improvement in Home Prices According to the S&P/Case-Shiller Home Price Indices

New York, September 29, 2009 – Data through July 2009, released today by Standard & Poor’s for its S&P/Case-Shiller1 Home Price Indices, the leading measure of U.S. home prices, show that, although still negative, the annual rate of decline of the 10-City and 20-City Composites improved compared to last month’s reading. This marks approximately six months of improved readings in these statistics, beginning in early 2009.

The chart above depicts the annual returns of the 10-City and 20-City Composite Home Price Indices. The 10-City and 20-City Composites declined 12.8% and 13.3%, respectively, in July compared to the same month last year. All 20 metro areas also showed an improvement in the annual rates of decline, with July’s readings compared to June.

“The rate of annual decline in home price values continues to decelerate and we now seem to be witnessing some sustained monthly increases across many of the markets” says David M. Blitzer, Chairman of the Index Committee at Standard & Poor’s. “The two composites and all metro areas are showing an improvement in the annual rates of return, as seen through a moderation in their annual declines.

Looking at the monthly data, the 10-City and 20-City Composites and 18 of the 20 metros areas increased in July. In addition, both Composites and 13 of the MSA have had at least three consecutive months of positive prints. These figures continue to support an indication of stabilization in national real estate values, but we do need to be cautious in coming months to assess whether the housing market will weather the expiration of the Federal First-Time Buyer’s Tax Credit in November, anticipated higher unemployment rates and a possible increase in foreclosures.”

More at link with formatted tables.

Futures down slightly this morning after a big up day yesterday.

DJIA INDEX 9,720.00 -8.00

S&P 500 1,057.40 -1.60

NASDAQ 100 1,716.50 -6.25

Today's economic calendar:

Redbook 8:55 AM ET

S&P Case-Shiller HPI 9:00 AM ET

Consumer Confidence 10:00 AM ET

State Street Investor Confidence Index 10:00 AM ET

4-Week Bill Auction 1:00 PM ET

Farm Prices 3:00 PM ET

Today's earnings reports:

Before open:

CPSL China Precision Steel, Inc. Basic Materials Steel & Iron

GIGM GigaMedia Ltd. Technology Internet Software & Services

NSSC Napco Security Technologies, Inc. Services Security & Protection Services

NTZ Natuzzi SpA Consumer Goods Home Furnishings & Fixtures

PBG Pepsi Bottling Group Inc. Consumer Goods Beverages - Soft Drinks

PCH Potlatch Corp. Consumer Goods Paper & Paper Products

THO Thor Industries Inc. Consumer Goods Recreational Vehicles

WAG Walgreen Co. Services Drug Stores

After close:

DRI Darden Restaurants, Inc. Services Restaurants

JBL Jabil Circuit Inc. Technology Printed Circuit Boards

LNDC Landec Corp. Basic Materials Synthetics

MDRX Allscripts-Misys Healthcare Solutions, Inc. Technology Healthcare Information Services

MLNK ModusLink Global Solutions, Inc. Technology Internet Software & Services

NKE Nike Inc. Consumer Goods Textile - Apparel Footwear & Accessories

PSEM Pericom Semiconductor Corp. Technology Semiconductor - Integrated Circuits

WOR Worthington Industries, Inc. Basic Materials Steel & Iron

ZZ Sealy Corp. Consumer Goods Home Furnishings & Fixtures

Monday, September 28, 2009

Market wrap - 5:20

Low volume up day for the market. Shot right out of the gate higher, then leveled off for the rest of the day.

Dow 9,789 124 1.28%

Nasdaq 2,131 40 1.90%

S&P 500 1,063 19 1.78%

Gold 994 +3 +0.25%

Oil 67.20 0.82 1.24%

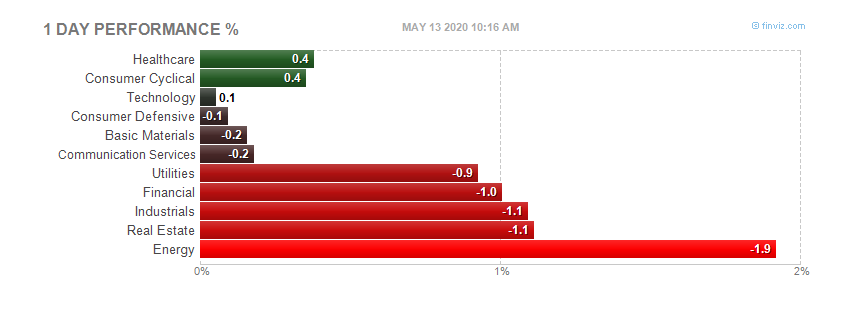

Today by sector:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Today's heatmap:

Pre--market, Monday, September 28, 2009

Futures up slightly this morning. Should be an interesting week.

DJIA INDEX 9,643.00 24.00

S&P 500 1,044.70 3.60

NASDAQ 100 1,702.50 5.50

Today's economic calendar:

4-Week Bill Announcement 11:00 AM ET

3-Month Bill Auction 1:00 PM ET

6-Month Bill Auction 1:00 PM ET

Today's earnings reports:

Before open:

CALM TRR

After close:

CRFT OHB

Subscribe to:

Posts (Atom)